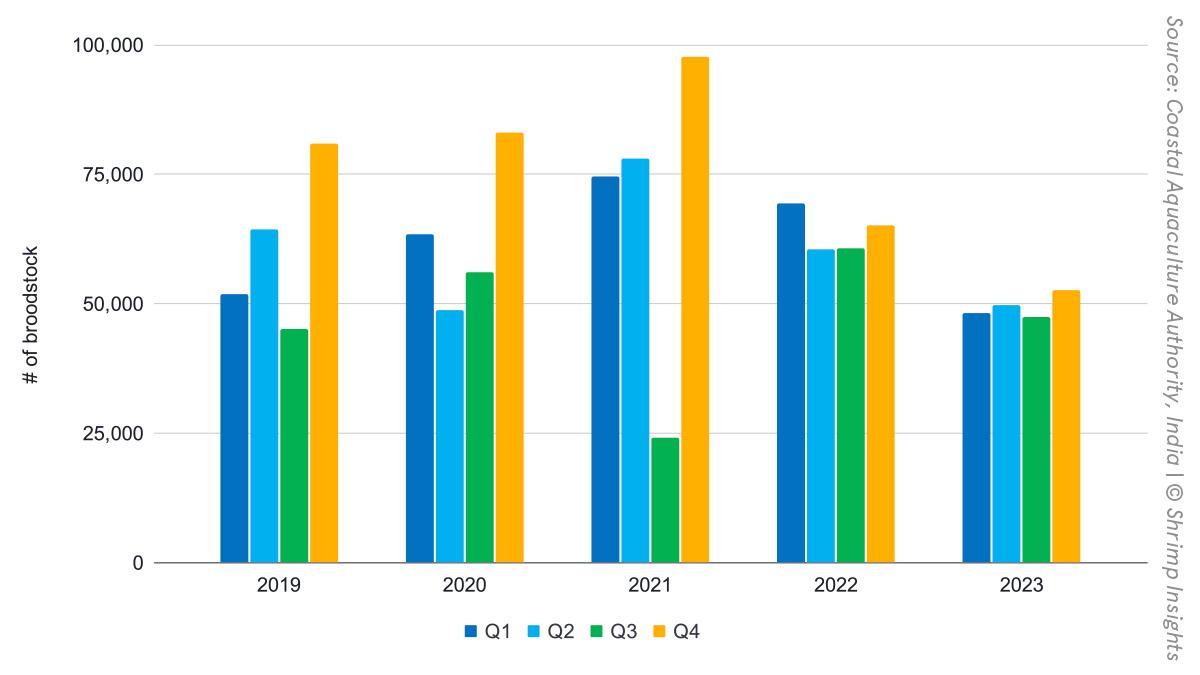

Although India’s year total L. vannamei broodstock imports and local BMC supplies have come down by 25% year-on-year, numbers from the last quarter of 2023 show some positive signs. In October, supplies still dropped by 48% year-on-year. However, in November and December 2023, L. vannamei broodstock supplies stabilized, and an equal number of animals compared to the same months in 2022 were supplied to the market. Although it’s a good sign that broodstock supply did not drop any further, the Q4 supplies are still 20% behind 2022 and even 45% behind 2021.

If we still take broodstock supplies as an indicator for future production, hatcheries are stocked to produce at least a similar amount of L. vannamei PL as in 2022. With farm gate prices showing some positive signs in January, it’s likely that PL demand will surge and that the market will absorb the hatcheries’ output during the first quarter of 2024. Although we might not see a year-on-year increase in production of L. vannamei shrimp during the first quarter (unless farmers go for much bigger sizes), we should not forget that total output may grow due to an increase in P. monodon production.

During the last quarter of 2023, India imported and locally produced 12,767 P. monodon broodstock, almost four times more than in Q4 2022. Notably, the hatcheries supplied with P. monodon broodstock also increased considerably. Vaishnavi’s hatcheries continue to expand their distribution of PL; seven hatcheries can now supply their Moana-powered PL to the market. Aquaculture de la Mahajamba continues to supply its hatchery, Unibio. But the company also supplied Gaayathri Biomarine, Golden Marine Harvest, and MAS Aqua Techniks. Lastly, the government's BMC has started commercializing its broodstock from the Andaman Islands and supplied BMR, CP India, and Royal Hatcheries for the first time. The broader availability of PL will certainly translate into a growth in output.

If we combine P. monodon and L. vannamei broodstock supply, the Q4 total supply would be only 4% behind 2022. If we look at November and December alone, the total broodstock supply would be 22% ahead of 2022. Again, if we take broodstock supply as an indicator of future production, we may expect an actual output surge during the first quarter of 2024. This does not necessarily mean an increase in exports as last year, it was believed that carry-over inventory from Q4 2022 was exported during Q1 2023. Considering 2023’s farming situation, this is less likely to be the case during Q1 2024.