The EU imported 376,875 MT of raw frozen Penaeus shrimp and value-added shrimp from Latin America, Asia, Africa, and the Middle East. This includes practically all farmed shrimp imports into the EU and excludes most wild-caught shrimp. 2024's import volume is 4% above 2023 and just 1% less than in 2022. Below are more details on EU 2024 imports (all restricted to raw Penaeus shrimp and value-added shrimp from Asia, Latin America, Africa, and the Middle East).

- Total

- December 2024: 28,481 MT = +12%

- Q4 2024: 95,669 MT = +3%

- Year-total 2024: 376,868 MT = +4% YoY and +26% to 2019

- Import Regions

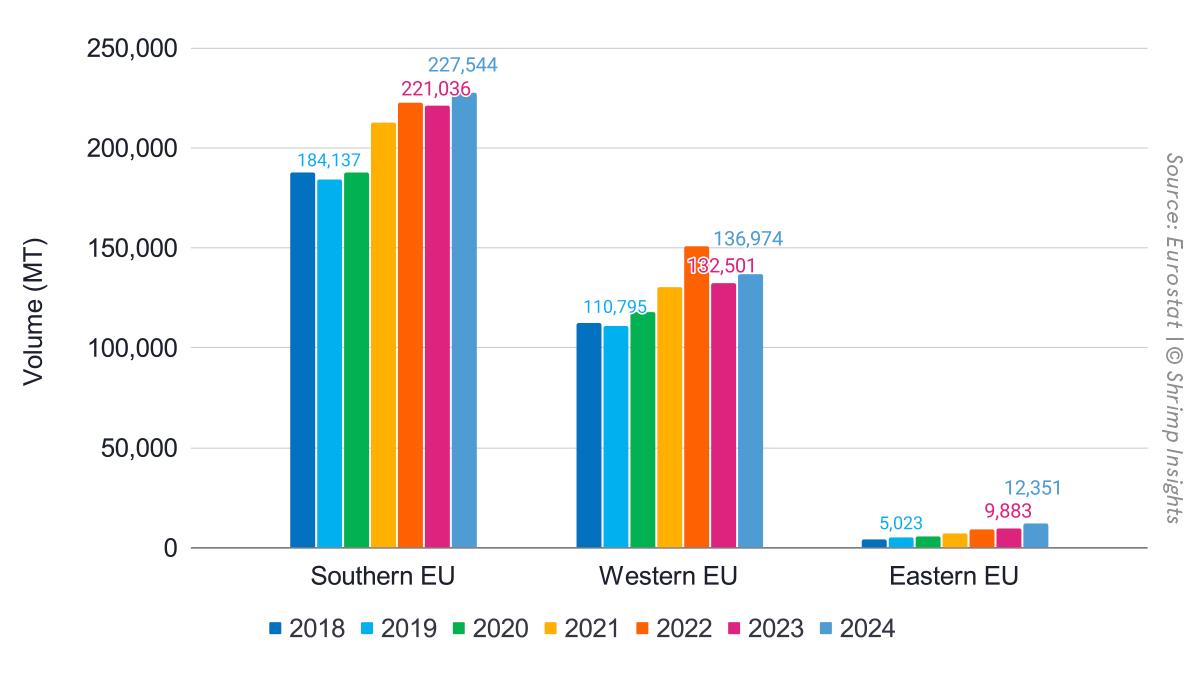

- Southern EU

- December 2024: 16,217 MT = +14%

- Q4 2024: 56,736 MT = +6%

- Year-total 2024: 227,544 MT = +3% YoY and +24% to 2019

- Northwestern EU

- December 2024: 11,291 MT = +9%

- Q4 2024: 35,939 MT = -2%

- Year-total 2024: 136,974 MT = +3% YoY and +24% to 2019

- Eastern EU

- December 2024: 973 MT = +28%

- Q4 2024: 2,994 MT = +5%

- Year-total 2024: 12,351 MT = +25% YoY and +146% to 2019

- Southern EU

- Products

- Raw Frozen Penaeus Shrimp

- December 2024: 24,050 MT = +8%

- Q4 2024: 82,220 MT = +0%

- Year-total 2024: 328,424 MT = +3% YoY and +31% to 2019

- Value-Added

- December 2024: 4,431 MT = +41%

- Q4 2024: 13,449 MT = +24%

- Year-total 2024: 48,445 MT = +13% YoY and +0% to 2019

- Raw Frozen Penaeus Shrimp

- Top Five Suppliers

- Ecuador

- December 2024: 14,186 MT = +16%

- Q4 2024: 44,706 MT = +2%

- Year-total 2024: 178,482 MT = +6% YoY and +78% to 2019

- India

- December 2024: 3,477 MT = -12%

- Q4 2024: 11,944 MT = +2%

- Year-total 2024: 46,280 MT = +4% YoY and +47% to 2019

- Vietnam

- December 2024: 4,870 MT = +38%

- Q4 2024: 14,156 MT = +21%

- Year-total 2024: 50,183 MT = +18% YoY and +2% to 2019

- Venezuela

- December 2024: 138 MT = -86%

- Q4 2024: 5,363 MT = -43%

- Year-total 2024: 38,866 MT = 0% YoY and +92% to 2019

- Bangladesh

- December 2024: 1,642 MT = +53%

- Q4 2024: 5,355 MT = +41%

- Year-total 2024: 13,510 MT = -6% YoY and -36% to 2019

- Ecuador

Some important observations:

While this year’s imports are a recovery from 2023 and put the EU almost at par with its record from 2022, the long-term growth trend is clear, with 2024’s import volume being 26% above 2019. The growth is equally driven by the South and Northwestern parts of the EU, which grew at +24% each over this period. The Eastern part of the EU is still small but grows much faster recording 146% growth compared to 2019.

While last year the imports of value-added items grew the fastest, the longer term trend reveals that growth has primarily been realized through the imports of raw frozen products. Value-added imports recorded 0% growth since 2019 while imports of raw frozen shrimp grew by 31%. This does not mean that value-added sales didnt grow faster. Some of the imported shrimp may be imported raw frozen, but processed in the EU to a value-added product.

In terms of suppliers, last year, Vietnam’s supplies rebounded to some extent, and imports from Ecuador and India grew moderately. However, looking at the longer-term trend, it’s clear that the growth of imports since 2019 has primarily been accounted for by Ecuador (+78%) and India (+47%). While Venezuela grew fast in the EU, imports in November and December stalled after Lamar Group’s farms and processing plants were nationalized. If Bangladesh does not stop its negative spiral, it will soon drop out of the top five suppliers in the EU.

The volume growth in 2024 has come amidst low prices for most of the year. However, since October, average import prices have increased quickly, and importers and exporters alike seem to feel comfortable that a higher price level will be established and maintained through most of 2025 due to healthier inventories.