The Shrimp blog is sponsored by Grobest, Inve Aquaculture, DSM Animal Nutrition, American Penaeid Inc., Zeigler Nutrition, Aqua Pharma Group, Mega Supply, and Undercurrent News.

Earlier this month, in a communication shared by Nitin Awasthi, seafood industry analyst at InCred Capital in India, that circulated among Indian industry insiders drew attention to India’s exceptional shrimp export performance during June and July 2021 and the possible strong demand for shrimp from the international market. Awasthi asked whether India was in the process of moving into an entirely new league if exports were to continue to outperform themselves.

For me, Awasthi’s publication triggered three questions:

1) How has shrimp production in India been performing in 2021 so far?

2) Will India be able to break its year-total export record?

3) Will a surge in supply of Indian shrimp be sustained by decent prices amidst strong market demand?

These questions are the focus of this post. To answer the first two, I talked to various insiders in India. For the third, I asked Gorjan Nikolik at Rabobank and Angel Rubio at Urner Barry their opinions.

The outcome of these discussions? I’m convinced that Indian supply may be met by strong demand and decent prices.

Pork and Beef Prices Have Gone through the Roof and May Cause a Surge in Demand for Other Proteins

Awasthi is optimistic that India’s exports will be met by a strong market. He believes we’re just at the beginning of a global protein rush to secure supply in which pork and beef are the major losers.

Awasthi draws attention to African Swine Fever (ASF) that is wreaking havoc in Asia’s pork industry, especially in China. China accounts for 50% of world pork production and for around 30% of global pork imports. ASF has caused a major shortage of pork and a surge in pork prices in China’s marketplace where pork makes up almost 40% of total land-based meat consumption. At the same time, Awasthi points to the news of mad cow disease (BSE) spreading in South America, a major beef-producing region, and China’s halt of imports of beef from Brazil. Being responsible for around 30% of global beef production, Brazil can cause major disturbance in the global beef market. With the shortages in beef and pork supply in mind, Awasthi is certain that the world is currently running short of land-based meat.

He believes that other protein sources must benefit from these shortages and that shrimp could be one of them. When reading all this, at first I had my doubts: normally, I wouldn’t think it possible for shrimp to compete with pork and beef. But then I talked to Nikolik and Rubio.

Shrimp Can Benefit from the Shortfall of Pork and Beef

The question of whether shrimp can benefit from a shortfall in beef and pork is something that Nikolik and his team has been debating for the last 2 years already. To a large extent, he shares my observation that price, taste, and consumption points are all very different for shrimp compared to the other animal proteins. He also thinks that the biggest winner from ASF will not be shrimp but poultry, which sells at a much lower price than shrimp.

But, he says, it’s much more complex than this, emphasizing that although he agrees with most of Awasthi’s observations, the main reason behind the sudden strong demand for shrimp is the food service segment opening up again on one hand while shrimp retail sales are still elevated on the other. But he does acknowledge that the other reasons cited by Awasthi definitely play a role in future demand too, such as ASF for pork and supply disruptions in the beef value chain.

In China, prices of pork have been so high at times and shortages so acute that seafood—and maybe even shrimp—has been seen as an alternative option (think of office canteens where a shrimp meal option suddenly looks more appealing when prices are similar). Nikolik wonders how one can ever explore this empirically, especially since there is a massive and convoluting effect of COVID-19. However, it’s clear that prices of pork and shrimp have become closer to each other and, particularly in China, this may result in increased demand for shrimp as a replacement for pork. With ASF still around, this situation doesn’t look like it will change anytime soon.

As for the US market, Nikolik thinks that 2020 has been a real game changer. Shrimp consumption in the US was already increasing moderately. But last year was, in a way, like a full year of promotions: retailers offered shrimp at low prices all year round. This stimulated at-home shrimp consumption big time, accelerating the ongoing increase of US shrimp consumption in general. Nikolik thinks that at-home consumption will remain above pre-COVID levels now that people have started to enjoy cooking shrimp at home. Combined with the shortage of other proteins, Nikolik thinks that we have the perfect scenario for people to try seafood—and especially shrimp—due to a price point that is now much closer to that of other animal proteins.

For Rubio, both Nikolik and Awasthi have no doubt hit the nail on the head when it comes to pork. For beef, though, he sees other reasons behind the upward price trend and supply shortfall. He explains that, on top of the reasons mentioned already, in the US both pork and beef continue to struggle massively from labor shortages; processing is very labor-intensive. Naturally, this issue has been exacerbated by the pandemic due to an even tighter labor market.

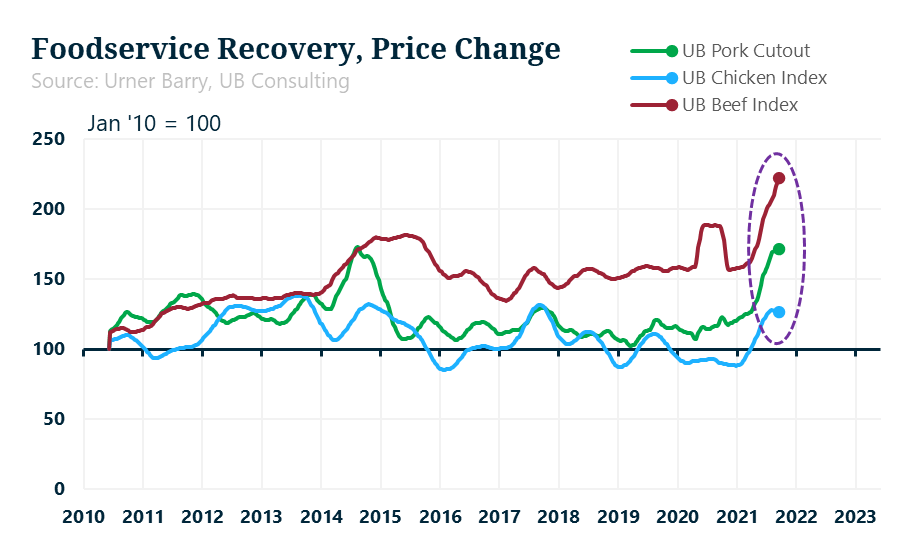

Figure 1: Example of price recovery of pork, beef and chicken in US Food Service

Source: Urner Barry Consulting

According to Rubio, other factors could also explain why prices for beef and pork are on the rise and reaching levels that are closer to shrimp prices. While last year shrimp was selling at very low prices, costs (labor, shipping, logistics) for other animal proteins have been rising rapidly. These rising costs have been passed along the distribution chain to the consumer. But in the US—and around the world in general—incomes rose dramatically last year. These conditions make for strong demand from consumers who’ve upgraded the type of protein they’re choosing… and they just keep on buying regardless of what the cost is (look at snow crab and lobster being sold at record prices despite good landings; or high-priced steak cuts). For now, as long as incomes remain high or increase even further, we might well witness an ever-stronger demand for animal proteins, including shrimp.

Talking to Nikolik and Rubio makes me think that shrimp might well see strong demand in the short- and mid-term future.

Let’s now look at India’s first half-year performance in 2021 and see whether it’s likely that India can continue to benefit from global demand. Can it keep up its performance all the way to the end of the year?

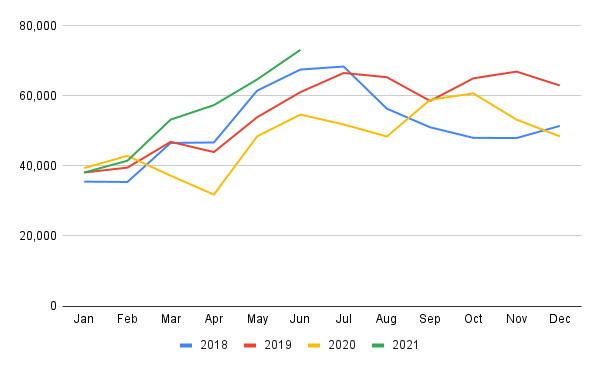

India’s Shrimp Exports Increased from 38,000 MT in January to 73,000 MT in June: A New Record

India’s 2021 shrimp export numbers so far are impressive. The monthly export volume has increased from 38,000 MT in January to 73,000 MT in June (figure 2). July export numbers are expected to have increased even further, maybe reaching as high as 80,000 MT. More relevant than the monthly numbers, as of March this year, year-total exports have been the highest ever seen. In June, the year-total stood at 328,000 MT, 19% higher than at the same time in 2018 which held the previous record for exports in the first half of the year.

Figure 2: India’s monthly shrimp exports (HS030617+160521+160529) from January 2018 – June 2021

Source: Government of India

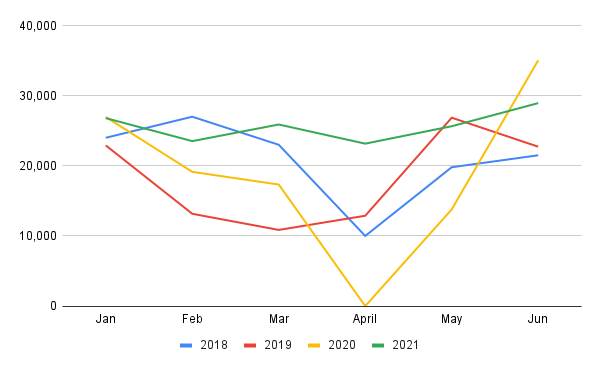

Interestingly, broodstock imports for the last few months of 2020 and the first half of 2021 (figure 3) seem to correlate with the peak in exports in May and June, and possibly July and August for which export data hasn’t yet been published. Broodstock imports during the first half of the year exceeded the volumes of 2018, 2019, and 2020 by 23%, 41%, and 27% respectively. Clearly this broodstock catered to the hatcheries producing PL for the summer crop, which turned out to be exceptionally good.

Figure 3: January – June broodstock import numbers for 2018-2021

Source: Coastal Aquaculture Authority

While broodstock import numbers may have already been a sign that a bumper harvest was on its way, talking to people in India reveals that the export record of the first 6 months of 2021 took many by surprise; most people believed that farmers, feed companies, hatcheries, and processors were still recovering from the COVID-19-related trouble experienced in the previous year.

According to some, the surge in output was a result of the silent expansion of inland shrimp farming in some districts in Andhra Pradesh. Others doubt whether those farms indeed harvested a lot, but rather point to bumper harvests during the summer crop in West Bengal and Odisha. It remains hard to get a real understanding of Indian shrimp production dynamics.

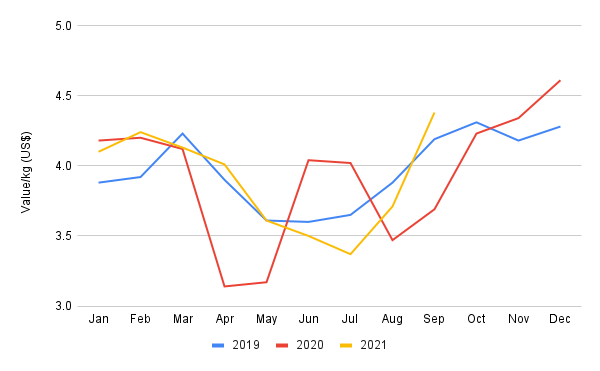

My feeling is that, in general, the relatively firm farm-gate prices at the beginning of this year (figure 4) may have encouraged farmers across the country to stock for the first crop, resulting in a strong harvest in May, June, and July; obviously, after a tough 2020, farmers were eager to try to go for a successful first crop in 2021, and they seem to have managed to do so.

Figure 4: Farm-gate prices for 60 count per kg in Andhra Pradesh, India (prices taken from the beginning of the month

Source: Seafood-TIP

Exports to the US Reached a New Record While Exports to China Stayed Just Behind the Record of 2018

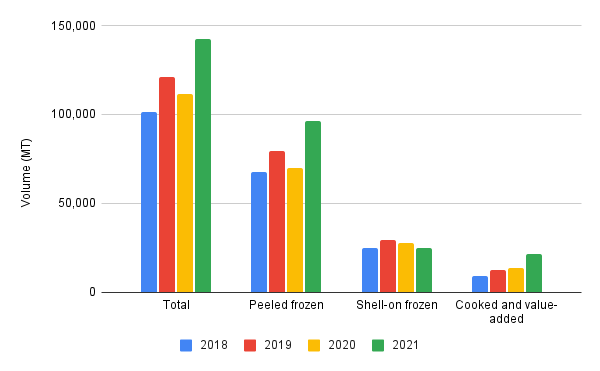

After a dip in exports last year, from January to June 2021 Indian exports to the US surged and easily outperformed not only 2020 but also 2018 and 2019 (figure 5). The total export volume almost touched 150,000 MT. It’s clear that US buyers have a renewed appetite for Indian shrimp, and India has definitely benefited from the reopening of the food service market. This is good news for most of the exporters in Andhra Pradesh which predominantly focus on the US market.

Figure 5: January – June US imports from India for 2018-2021

Source: NOAA

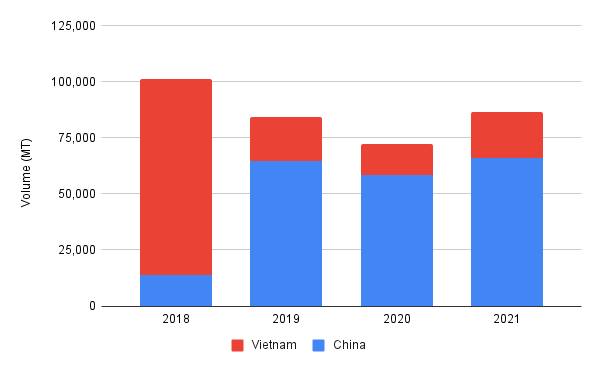

Also exports to China (both combined and separate from exports to Vietnam) are on the rise again (figure 6). Despite all the news about political tensions between the two governments, COVID-19-related port closures, and rumors about 1,000 Indian containers being stuck in Chinese ports, in the first half of the year Indian exports to China recovered and, while still behind 2018, outperformed 2019 and 2020. Despite all the issues in China and between China and India, it seems that China’s reprocessing industry has also regained its appetite for Indian shrimp. This is good news for India’s exporters focusing on headless shell-on (HLSO) bulk business.

Figure 6: January – June exports from India to China for 2018-2021

Source: Government of India

Some people believe that demand for the second half of the year may slow down because part of the first half year’s rush was due to importers trying to replenish their stocks. I doubt whether they’re right. I keep in mind the container shortages in Asia and the fact that many importers—especially in the food service segment—in Europe, the US, and China are still busy replenishing their stocks. Bearing in mind these low inventories combined with strong market demand for all animal protein products, I'm pretty sure that Indian exporters will see good demand for the months to come.

Is India Moving into a New League or Is Its Export Performance Just Getting Back on Track?

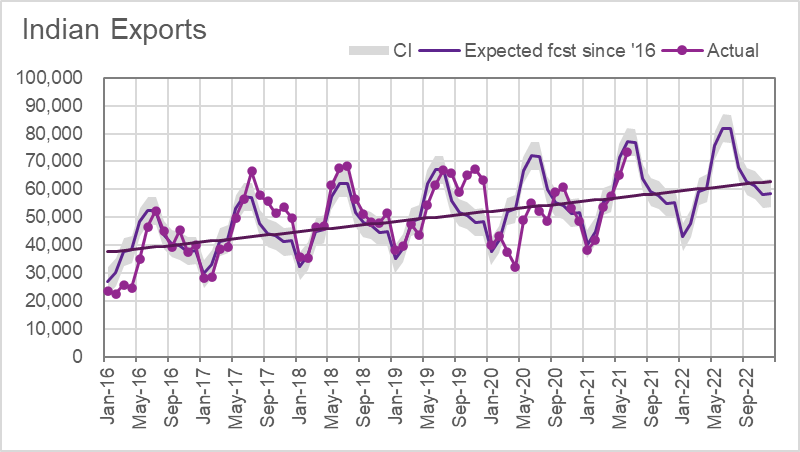

In his post, Awasthi states that India would move into an entirely new league if 80,000 MT in July would be reached, and a new year-total export record would be realized. So, I asked Rubio his opinion, and he ran some statistics for me.

Figure 7: Angel Rubio’s statistical analysis of India’s shrimp export trend from 2016 – present

Source: Urner Barry Consulting

Rubio argues that it all depends on how you look at it. Based on the historical trend from 2016 till today, an export volume of 80,000 MT in July—although an export record in itself—would be within the boundaries of what Rubio would have expected to see as Figure 6 shows. But, of course, 2020 was a year in which we saw Indian exports decline due to COVID-19, and if you were to take a shorter time frame for analysis (e.g. 2018), then suddenly 80,000 MT would be out of the boundaries of what could be expected. I think that if we assume that 2020 was an anomaly due to COVID-19 and not due to structural factors, it’s fair to look at the time frame from 2016 till today. And in that case, instead of moving into an entirely new league, India is back on track and is increasing its shrimp exports as we might have expected.

I then wonder whether we might come to a different conclusion if we were to look at this year’s year-total exports from January till June and compare that with previous years. Delayed harvests and shipments in April and May due to COVID-19-related labor and container shortages may, at least partly, explain the high export numbers in June and July. Therefore, June and July’s export numbers might not be entirely representative for what happened on the production level.

Figure 8: Angel Rubio’s statistical analysis of India’s shrimp export trend from 2016 – present

Source: Urner Barry Consulting

According to Rubio, even though this year’s year total is indeed at a record high in absolute terms, if you look at the annual growth rate and forget 2020’s exports but instead compare this year with 2019, this year’s growth rate of 15.6% is not a new record (figure 8). Exports grew faster in 2017 and 2018. So, although in absolute terms India is definitely breaking records, looking at growth, this first half year’s export performance is not yet placing India in an entirely new league.

Stocking of the Second Crop Delayed and Supply Not Expected to Surge Before Mid-October

Whether India will break records at the end of this year depends on how well the remaining crops will perform.

When harvests peaked from May till July, a drop in farm-gate prices followed. It was only in August that prices started to surge again. During the same period, feed prices were on the rise due to high raw material prices, which caused feed producers to transfer part of this cost to the farmers. As a result, farmers were reportedly unwilling to stock their ponds. And even if they had wanted to stock, there would likely have been a shortage of PL due to a 2-month break in broodstock imports enforced by the Coastal Aquaculture Authority because of maintenance of the import facilities. All these factors combined have resulted in the current low supply situation that has caused prices to rise. At the time of writing (mid-September), farm-gate prices are at even higher levels than we’ve seen in the previous 2 years (Figure 3), and I can’t think anything other than that farmers will be eager to stock their ponds if the weather allows it.

Photo 1: Recent flooding in Jagatsinghpur in Odisha doing damage to shrimp farms

Source: Posted on LinkedIn by Rabi Narayan of Pasupati Agrovet

Even with the current stocking going on—or that expected soon—it’ll probably get to the end of October before larger volumes of shrimp are available again. Therefore, I do expect that export numbers for September and possibly also October will show a significant drop compared to the previous months, when exporters were processing and shipping the harvest from earlier in the year. So, if 2021 is to become a record year, November and December will have to reach 70,000-80,000 MT again. If not, 2021 will stay behind 2018 for sure.

There are a couple factors that may have a negative impact on production in the remainder of 2021. West Bengal has not yet recovered from earlier cyclone damage and not much shrimp will be stocked or harvested. Also, many sources in India report diseases having a serious impact on production in Andhra Pradesh. However, I continue to have a hard time believing that disease will cause a significant drop in total production: farmers increasingly know how to deal with disease and tend to harvest smaller sizes before mortality strikes. I also think that any decline in production in existing farms could well be outweighed by an increase in production from new farms. With these points in mind, I wouldn’t be surprised if India does indeed break its previous year-total export record.

Whether Volume Increases or Not, Indian Farmers Are Likely to See Decent Prices

The situation in India remains hard to read as different people have different reasons to make us believe that supply will be abundant or scarce. But one thing is sure: whether India is moving into a new league and can continue to increase its output or not, India’s shrimp farmers may expect decent prices for their shrimp harvest, probably until the end of the year or even the first crop of 2022.

It’s not only the protein rush and the shortage of beef and pork that are stimulating prices, but also a shortage of peeled shrimp supply from countries like Vietnam and Indonesia, which are still battling COVID-19. If India’s farmers have managed to stock their ponds and can start harvesting considerable volumes towards the second half of October, they may well be rewarded by relatively high market prices.