Whether you like it or not, consumer awareness surrounding sustainability as well as social and animal welfare issues in food supply chains is rising. Many of the sustainability issues are covered by third-party certification programs such as Best Aquaculture Practices (BAP), Aquaculture Stewardship Council (ASC), and GLOBAL G.A.P. Other certification bodies deal with social issues in processing facilities and the wider value chain. But animal welfare is only covered to a limited extent by these existing certification schemes.

Many of us in the industry assume that having several of these certifications in place is sufficient. But at the Global Shrimp Forum (GSF) which took place from 6-8 September in Utrecht, the Netherlands, Hugo Byrnes (until recently VP of Product Integrity at Ahold Delhaize, one of the world’s largest food retailers with investments in Europe, the US, and Asia) made it clear that it’s time for the shrimp industry to wake up to the fact that certification alone is no longer sufficient; it will take more to comply with future regulations and additional buyer requirements.

In this post I’ll go through some of the topics currently on my radar about sustainability, and social and animal welfare issues that are sure to need your attention moving forward. I want to challenge you to not see all of these developments as a burden, but rather view them as opportunities to create a competitive edge for your shrimp in the protein marketplace.

The Shrimp Blog is supported by: Inve Aquaculture, Benchmark Shrimp Genetics, Shrimp Improvement Systems, SPF Shrimp Feeds, Megasupply, DSM Animal Nutrition, Taprobane Seafood and Verwijs Import, Zeigler Nutrition, and Grobest.

ANIMAL WELFARE ISSUES RAPIDLY GAINING ATTENTION

While sustainability and social issues have been on all of our radars for a while, animal welfare issues have only become more prominent recently. That’s certainly the case for me, and possibly also true for you too. The two main issues commonly raised are (1) animal-friendly slaughter, and (2) eyestalk ablation.

It’s now clear from the science that fish feel pain, but there isn’t yet the same substantial scientific evidence that shrimp feel pain. However, some organizations say that this evidence is rapidly evolving, and papers providing such evidence will be published soon. Looking ahead, Hilton Foods (supplier of seafood to Tesco, the UK’s largest food retailer) has already started to use electrical stunning in its shrimp supply chain. But the overall willingness of the industry to adopt electrical stunning is so far limited as it’s viewed as expensive and an additional burden for the harvesting teams. If the scientific evidence grows, retailers will increase pressure on the industry to make slaughter more humane. Whether electrical stunning becomes the method of choice is not yet clear. But what is very clear to me for one is that we have to prepare ourselves for more discussion and debate about this topic in the future.

Note: Although the language of this program is Dutch, it’s worth watching from 18:45 min where you can see a visit to a Thai hatchery, parts of which are in English. (Click on the image to open in a new tab.)

Today, eyestalk ablation is an urgent issue, and abolishing such practices could well become a market access requirement in some markets soon, such as in the northern Europe market. This month, a popular Dutch TV show featured an item about eyestalk ablation (see Video 1) on national television. They showed the process of eyestalk ablation in a hatchery in Thailand, how the hatchery technician uses heated scissors to cut the eye of the female breeder, and how it then twitches before being put back in its tank. This type of negative attention on the process is perceived by retailers in the Netherlands and other parts of Europe as being a reputational risk, and if not dealt with it may result in less shrimp on the shelves. At the GSF, Byrnes announced that already in 2022 Ahold Delhaize will start making it a requirement that, for some of its supermarkets, the shrimp will be produced without the use of ablation.

One important nuance with regard to eyestalk ablation is that if wrongly framed by journalists or activists, consumers may believe that all farmed shrimp have been ablated, and this is not the case. Shrimp-breeding companies that still use ablation only use it with the post-larvae-producing females (PL) that farmers then buy to, in turn, produce the shrimp that is then processed into the products that end up on consumers’ plates. The result of ablation is that the female will spawn more eggs, reducing the number of breeders that a company needs to produce its required volume of PL. This doesn’t necessarily make it much better, and if hatcheries can produce without ablation they should start doing so, but it’s an important nuance: there’s a huge difference between the number of shrimp that actually undergo ablation and suffer from it, and what is often commonly cited in the media.

With public attention for eyestalk ablation on the rise, certification bodies have it on their radars as well. Eyestalk ablation has been prohibited by the EU organic standard for many years, and from 2024 GLOBALG.A.P. will require that PL are produced without ablation—it’s only a matter of time before the other certification standards follow.

RETAIL COMMITMENTS TO REDUCE SCOPE 3 EMISSIONS

In his presentation at the GSF, Byrnes addressed the fact that Ahold Delhaize has committed to a 15% greenhouse gas emissions reduction by 2030 (against a 2018 baseline) becoming net zero across the entire supply chain, products, and services no later than 2050 and working to a 1.5-degree trajectory in line with science-based targets for its scope 3 emissions. These targets concern emissions related to the extraction of raw materials for Ahold Delhaize’s products, the manufacturing of the actual products, and the transportation of these products to distribution centers.

Ahold Delhaize isn’t alone. Berry Marttin, member of the Managing Board of Rabobank Group, in his presentation at the GSF showed that worldwide around 15% of retailers have committed to reducing scope 3 emissions. In specific markets such as the UK (60%), Australia (40%), North America (35%), and the Netherlands (30%), this percentage is much higher.

As Byrnes told the GSF, retailers with commitments need to think about how food is farmed and eaten, and how forests and carbon sinks are managed. But retailers can’t do this on their own. While they need to produce their own roadmaps and integrate the economics into their business models, they must also work with their suppliers to gather emissions data and set reduction targets, and find the best solutions to reduce emissions in all of their supply chains.

Farmed shrimp supply chains are also part of this. Importers, exporters, farmers, feed companies, and others that are part of these retailers’ supply chains with scope 3 emissions targets will soon have to start mapping emissions in their supply chains and make plans to reduce them. Several organizations, such as DSM Animal Nutrition with its Sustell™ service and the Sustainable Trade Initiative (IDH) with its Aquaculture Working Group on Environmental Footprint are developing tools that can, as a first step, help with mapping the carbon footprint of farmed shrimp supply chains.

CAN SHRIMP BECOME A CARBON NEUTRAL OR CARBON NEGATIVE SOURCE OF PROTEIN?

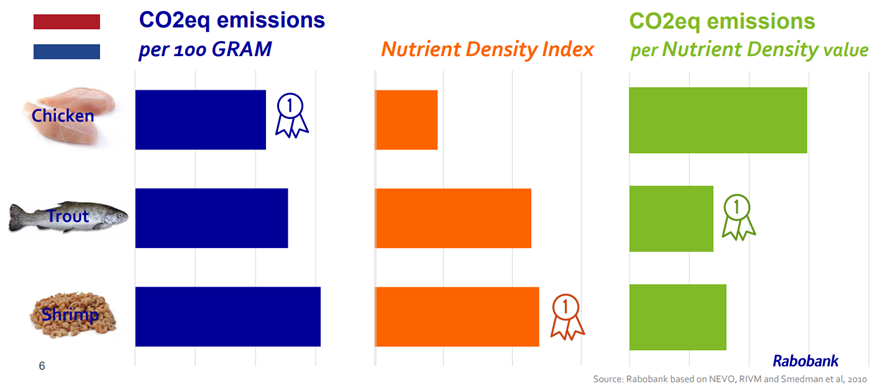

During his keynote speech at the GSF, Berry Marttin, member of the Managing Board of Rabobank Group, pointed out that we need to make sure that we use the right metrics when looking at how shrimp compares to other proteins in terms of its emissions. Figure 1 shows data for wild-caught shrimp, but the principle can also be applied to farmed shrimp, which is what we’re interested in here. Figure 1 shows that while in terms of the carbon dioxide equivalent (CO2eq) per 100 g of protein shrimp might turn out to be a less sustainable option than, for example, chicken or trout, if we were to look at it relative to its nutrient density, farmed shrimp might suddenly be a much better option than chicken and almost equally as sustainable as trout.

Note: The data used in Figure 1 is for wild-caught shrimp.

Although the numbers in Figure 1 don’t reflect the most recent data, more thoroughly investigating the carbon footprint of farmed shrimp may be crucial as part of a strategy to better position shrimp as a sustainable protein choice. This is especially true when, in the future, costs such as the environmental footprint of products or costs related to unhealthy diets will be calculated into the prices consumers pay for their products.

If shrimp could actually become carbon negative, if shrimp farmers were to generate carbon credits by replanting mangroves, for example, the shrimp industry could even generate additional income. Reforesting mangroves would generate carbon credits that could be sold to businesses that need to offset their emissions. This would, in turn, help the industry to become more competitive in comparison with its less sustainable peers. Need more inspiration? Check this out: https://www.thebluecarboninitiative.org/about.

SUSTAINABLE MARINE AND ALTERNATIVE FEED INGREDIENTS

One of the major—if not the most important—sustainability challenges faced by the shrimp industry, and something that’s on many food retailers’ agendas, is the amount of feed, as well as the feed ingredients used, to grow the shrimp. Whether plant-, marine-, or terrestrial animal-based, all ingredients have their own set of associated risks and challenges. Although certification bodies such as ASC, BAP, and GLOBALG.A.P. have feed standards that their certified suppliers have to comply with, there are some food retailers in the market who want to take it a step further.

The three main areas that food retailers would consider tightening the requirements for are (1) reducing the dependence on marine ingredients, (2) ensuring that remaining marine ingredients are sourced from sustainable origins, and (3) the traceability of ingredients.

First of all, it’s about reducing the dependence of shrimp feed manufacturers on marine ingredients, other than the trimmings of fish processing facilities. It’s a general perception that to be considered as a sustainable source of protein, the amount of fish used to produce a kilogram of shrimp (Fish-In:Fish-Out or forage fish dependency ratio) should be reduced as much as possible by using alternative feed ingredients. This was also a topic that Prof. Kevin Fitzsimmons presented at the GSF back in September.

Video 2: Calysseo’s (a joint venture between Calysta and Adisseo) started operating in late 2022 and will produce 40,000 MT of single-cell protein, which has high potential to become an ingredient for shrimp feed. Source: YouTube.

While there are undoubtedly many less sexy alternative feed ingredients, the three most popular categories being talked about right now are: insects (companies such as Protix in the Netherlands, Innovafeed in France, and Entobel in Vietnam); single-cell proteins (companies such as Calysta in the US/China, and KnipBio in the US); and algae (companies such as Veramaris and Corbion in the Netherlands). While still in the early stages of development, the number of companies involved in the alternative feed ingredient space is growing rapidly, and the first real industrial production sites are up and running in different parts of the world.

Video 3: Innovafeed is one of several large-scale black soldier fly protein producers that has industrial production sites up and running and capital available for further expansion. Source: YouTube.

The marine ingredients that are still used in shrimp feed—the complete replacement of feed ingredients today not being considered feasible or desirable for most feed manufacturers—should subsequently come from sustainable origins such as an MSC- or MarinTrust-certified fishery or, even better, from processing the by-products (trimmings) of such fisheries. Whether by-products from processing or not, marine ingredients should be traceable as far back to their origins as possible. The Seafood Task Force and its members are even thinking about making it mandatory for shrimp feed manufacturers to be able to trace the fishmeal and oil components of the feed back to the boat that caught the fish used to produce the meal and oil. In many cases, this level of traceability is at present hard to achieve, but looking at how consumer demand and regulatory requirements around transparent supply chains are evolving, it’s not unlikely that such data will have to be provided in the future.

BUILDING CULTURES OF SUSTAINABILITY

We could view the EU and US markets, and specific retailers in those markets, as being outside of reality: who will pay for all the extra costs associated with making shrimp production fully sustainable, as well as fully responsible in terms of animal welfare and social issues? But the reality might be that in a future where consumer awareness around sustainability, social issues, and animal welfare will only continue to rise, proactively integrating all of these issues into our practices may well give shrimp that competitive edge it needs to become a protein of choice for larger groups of consumers around the world. And such an approach could, in turn, create the demand for farmed shrimp that is needed for markets to absorb the projected significant increases of shrimp production from Latin America, Asia, and other parts of the world.

Instead of seeing these issues only as burdens, we can choose to look at how we can use them to give us our competitive edge. And as Walter Faaij told us recently at the GSF, for this to happen we need to build a culture of sustainability within our industry and develop a tribe of front-running companies that take the lead.