Oh boy, has the shrimp market been difficult to read. In this blog, I will reflect on whether my forecasts about the impact of Covid-19 on global shrimp demand and supply have been right or wrong. It was, and still is, so hard to read the shrimp market in such a period of global crisis. Writing this blog has enabled me, and hopefully also you, to get a better grasp of what has been happening in the marketplace.

THE SHRIMP MARKET HAS BEEN A ROLLER COASTER WITH DIFFERENT TRAJECTORIES FOR EACH MARKET

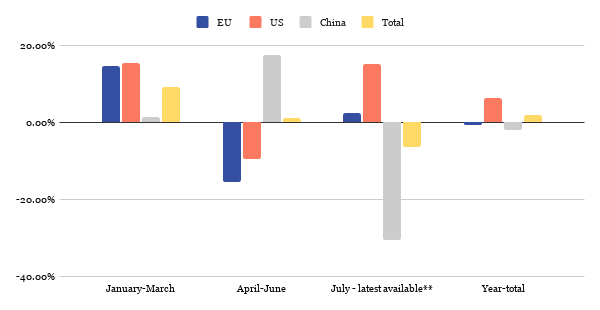

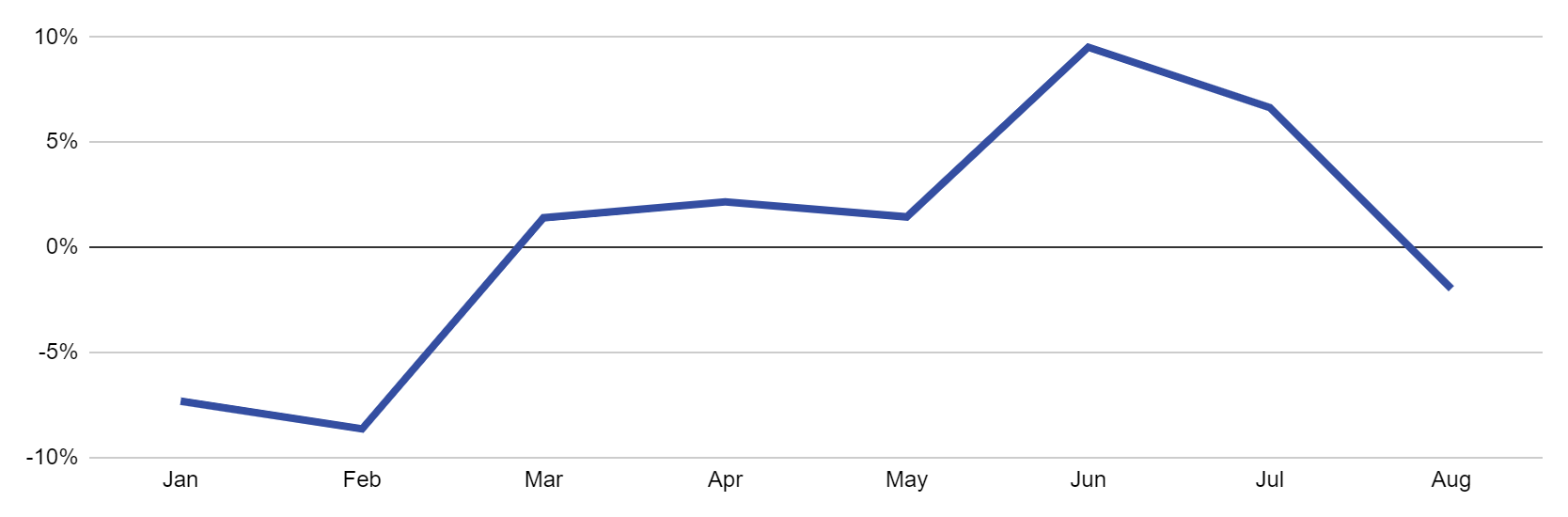

Figure 1 shows us the year-on-year growth rates of imports of the three main markets – the EU, the US and China. The EU and the US both saw a very strong start of 2020. Although China only increased its imports slightly, the total growth rate of the three markets combined during the first quarter was almost 10%. China went into an earlier lockdown than the EU and the US, and this is clearly reflected in the figures. Comparing the first and second quarter of 2020 (see Figure 1), the import situation for the EU and the US on one hand, and China on the other, is almost completely reversed. While China was finding its way back in April-June and saw its imports increase by 18%, imports in the EU and the US dropped by 16% and 9%, respectively.

Figure 1: Year-on-year growth rates for the EU*, the US and China

Source: EUROSTAT, NOAA, Chinese customs

Notes:

* In this blog I have only included EU imports of HS03061792, which is limited to raw and blanched HOSO, HLSO and peeled Penaeus shrimp (largely accounted for by L. vannamei). For China and the US, this blog includes all warmwater shrimp imported under HS030617, which can also include some wild-caught warmwater shrimp not belonging to the Penaeus species.

** July is the latest available data for the EU, while August is the latest available data for the US and China.

In July and August, however, the situation turned 180 degrees – again. Due to Covid-19 detections in Ecuadorian cargo, China’s imports tumbled and declined by 30% compared to the same months in 2019. Even though imports for US retail jumped and the US even recorded 15% growth in July and August 2020 compared to the same period last year, this wasn’t enough to balance out the total import volume of the three markets. Total imports of the three markets combined, in the third quarter of 2020, fell behind 2019 by 6%. In August, the year’s total imports of these three markets was now only 1% ahead of 2020. Keep reading, and we’ll see what happened in each of these three markets in more detail below.

AFTER A CRASH IN APRIL AND MAY, EU IMPORTS RECOVERED IN JUNE AND JULY

Back in June, after an initially good start of 2020, I expected EU shrimp imports to fall from April onwards. While EU imports in March were still 15% ahead of 2019, in April the first cracks appeared (as seen from Figure 2 and 3). Italian imports declined by 44% (compared to May 2019) and north-western Europe’s imports (composed of the Netherlands, Belgium and Germany) dropped by 17%. In May, mainly driven by a further dive of imports in hard-hit southern Europe, the situation got even worse and imports went down by 36% compared to May 2019.

Figure 2: Volume (MT) of EU (excl. UK) imports of warmwater shrimp (HS03061792)

Source: EUROSTAT

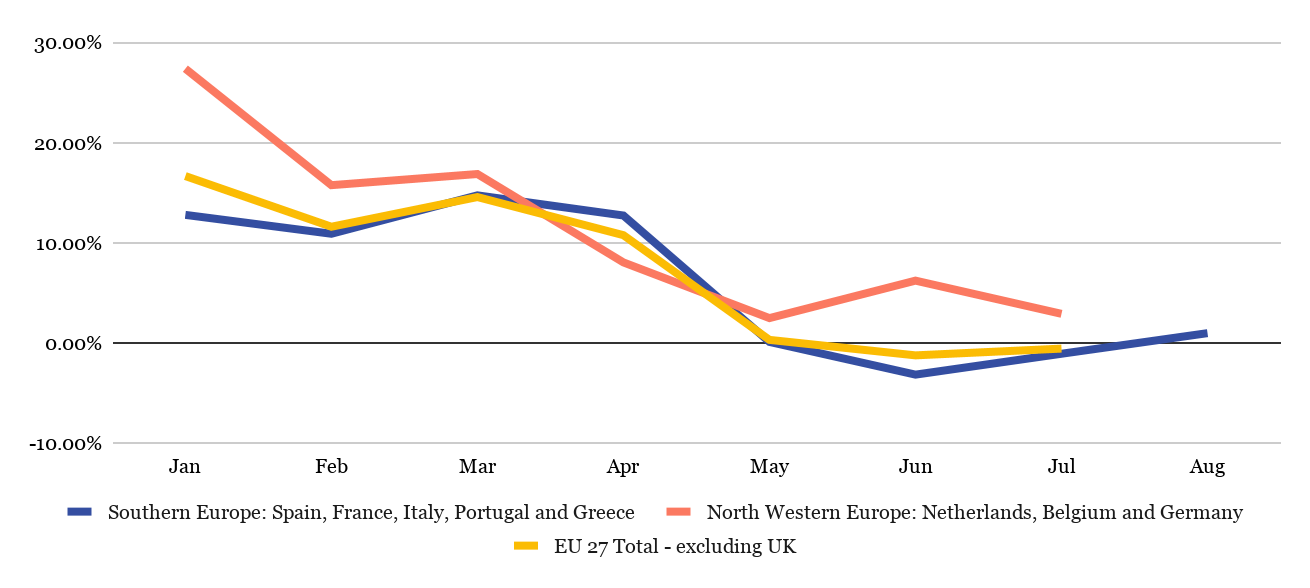

Figure 3: EU (excl. UK) year-to-date total growth rate 2019-2020 (HS03061792)

Source: EUROSTAT

Although I expected that imports would dive more strongly in June, imports were down by only 9% compared to June 2019. Imports in Italy (-77%), Spain (-42%) and Germany (-16%) showed negative growth, but Portugal (81%), France (36%), the Netherlands (59%) and Belgium (4%) showed positive growth. In July, the situation improved further and EU imports exceeded July 2019 imports by 2% (Figure 2). In June and July 2020 (Figure 3), the EU year-to-date total imports were only 1.2% and 0.6% behind the year-totals of June and July 2019.

My first thought was that retail sales must have been stronger than I had expected and compensated for wholesale. However, it turns out that not only retail performed well but also restaurants had a much better summer than I had anticipated. Restaurants in the EU were allowed to reopen from May and June. To prevent overcrowded situations, restaurants expanded outdoor terraces. Consumers spending their holidays at home were dining out more often than they would normally do. Due to this jump in demand from the restaurants, by the end of August, many wholesalers had largely made up for their losses in April and May and, thanks also to the strong start of 2020, were still ahead of 2019.

While many wholesale suppliers cancelled containers in the early days of the crisis in April, a lot of them also replaced these orders in May and June when they saw the quick recovery. As a large part of inventory was sold during summer, many importers hurried to place new orders in August and September. The importers I spoke to said that, although they placed new orders to replenish their stocks, they remained cautious. They expected that wholesale sales would slow down when restaurant visitors would not be able to sit outdoors any longer due to colder weather. None of these importers had however foreseen another closure of restaurants, which is what is now happening across the EU.

The outlook for the EU shrimp market for the remainder of 2020 has turned bleak. Even though new lockdowns seem to be shorter and more localized, once lifted, stringent measures limiting the number of guests that restaurants are allowed to accommodate are likely to remain in place. Maybe even into 2021. Contrary to earlier this year, it is unlikely that European importers cancel their orders. This time, importers will be placing the products in cold storage. It is likely that the inventories that are now being built and were initially ordered to service the autumn and winter seasons, may actually last as far as Easter 2021.

US RETAIL SHRIMP SALES INCREASED BY OVER 50% BETWEEN APRIL AND JULY

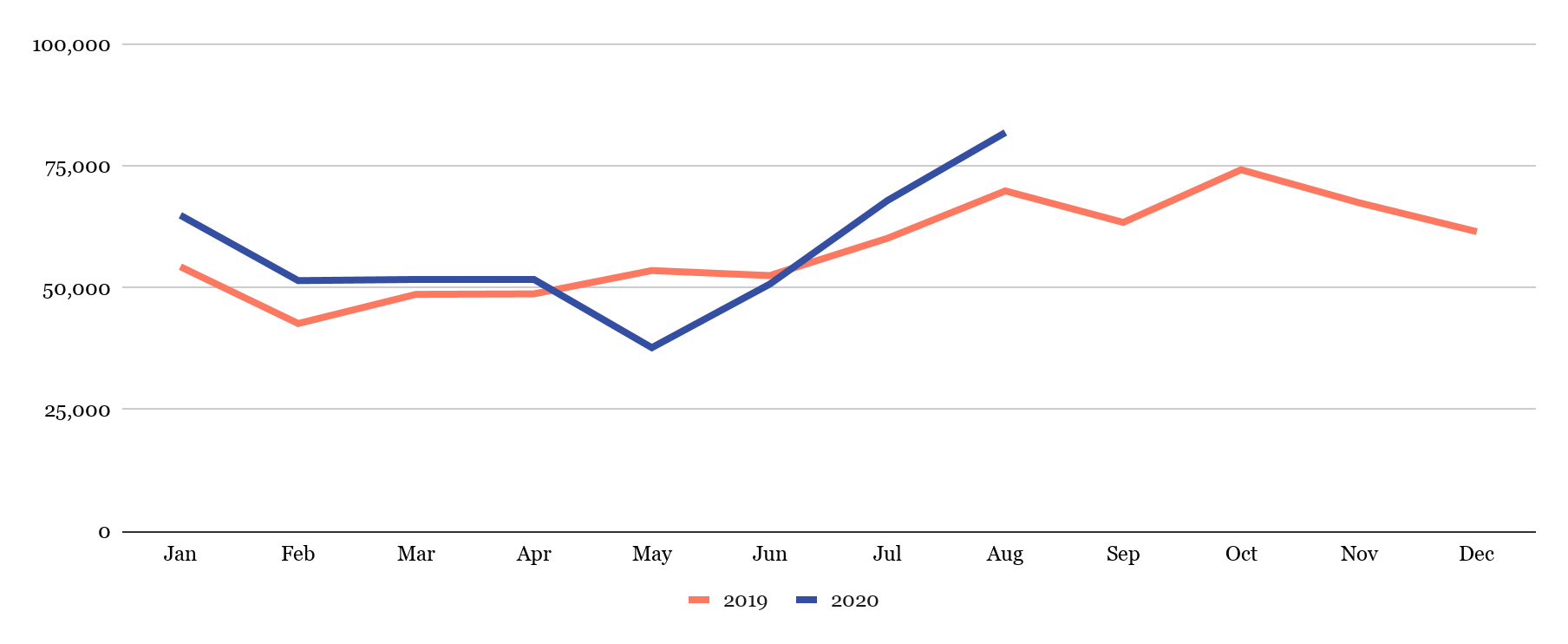

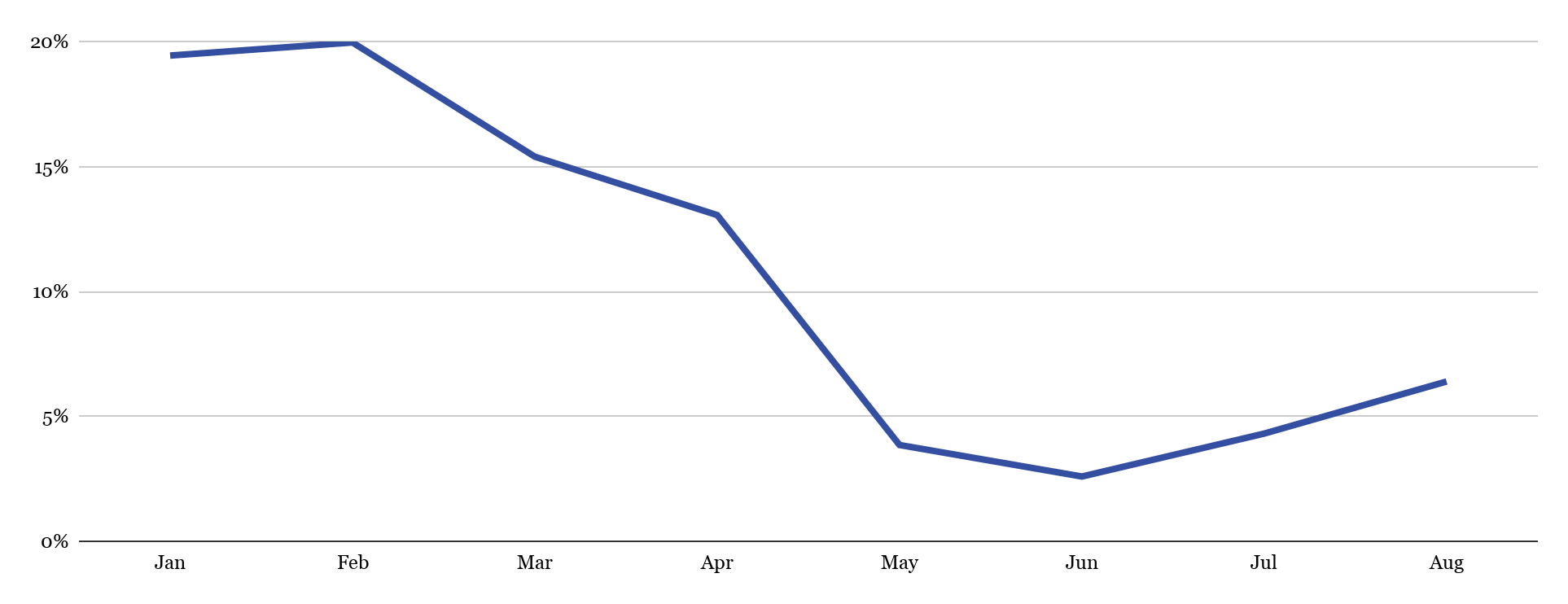

In April, the US was still 13% ahead of its 2019 imports, but this number dropped to 4% in May and to 3% in June (Figure 5). In May and June, imports dropped by respectively 30% and 3% compared to the same months in 2019 (Figure 4). While I expected this drop to last longer, imports recovered rapidly in July and August and even grew 13% and 17% compared to the same months in 2019. In August, the US – somewhat surprisingly – imported its largest amount of shrimp ever: 82,000 MT. The year-to-date total imports in August were around 458,000 MT, 6% above 2019. Despite Covid-19, or maybe thanks to Covid-19, the US may be heading for another record year.

Figure 4: Volume (MT) of US imports of warmwater shrimp

Source: NOAA

Figure 5: US year-to-date total growth rate 2019-2020

Source: NOAA

According to the National Fisheries Institute, shrimp is the most consumed seafood in the US and in 2018 consumers ate more than 2.1 kg per person on average. Before Covid-19, around 75% of shrimp was sold to restaurants. Retail only accounted for 25% of shrimp sales. With this in mind, I expected imports to decline rapidly when restaurants throughout the US closed. But reality proved to be different.

Urner Barry’s shrimp analyst, Angel Rubio, showed in a recent seminar that retail sales have already been growing steadily for a couple of years. This year, however, they exploded. From April to July 2020, retail sales increased by 57% in volume and more than 60% in value. Rubio explains that the sudden closure of a large part of the wholesale segment created a demand shock and resulted in an unprecedented growth in the retail segment. Retailers encouraged consumers to buy shrimp by running promotions. Rubio explains that retailers could do this because they were trading at high margins: with the wholesale segment paralyzed, they were the only ones buying shrimp. Although increased retail sales have been at least partially responsible for the US’s recovery of imports, there may also be other explanations.

Just like in the EU, after stringent lockdowns ended, consumers in the US were more than happy to go out for dinner. Restaurants opened large terraces to serve dinner outdoors. Staying at home during the holidays, consumers dined out more often than usual. On top of that, various companies in the food service segment who were already introducing innovative concepts encouraging at-home delivery of seafood meals accelerated their plans and this way contributed to increased shrimp consumption. So in the US, too, wholesale sales recovered much faster than I had anticipated.

However, Jeff Sedeca, president of Sunnyvale Seafoods, warned at an Undercurrent News webinar in September that retailers in the US sell different products than wholesalers. According to him, where retailers sell significant volumes of peeled products, wholesalers sell mainly headless shell-on (HLSO) products. So while increased retail sales caused more demand for peeled products, there might actually at the same time have been an oversupply situation of HLSO products for the wholesale market. Most of the products imported at the start of the year were wholesale products. The rapid increase of retail sales caused demand for a different type of product. New orders of retailers are likely the driving force behind the large volumes of shrimp we’ve seen entering the US market in recent months. There might be considerable inventories of unsold wholesale products waiting in the cold stores for restaurants to start ordering again.

US restaurant consumption during the winter season will be limited due to Covid-19 restrictions on restaurant occupancy and cold weather that prevents outdoor dining. I’m afraid that restaurant consumption is unlikely to rise again to pre-Covid-19 levels before Easter or spring 2021. With all this in mind, US imports in the first quarter of 2021 might really slow down this time.

CHINESE LIFE WENT BACK TO NORMAL BUT COVID-19-RELATED SHRIMP SCANDALS PUT THE MARKET AT RISK

China recorded negative growth rates in the first two months of 2020 and, already in February, was almost 10% behind 2019 (Figure 6). Imports recovered from March onwards and, as of that month, even outperformed 2019. In June, imports were higher by almost 10% (Figure 7). Imports only started dropping in July, when Ecuadorian cargo was tested positively for Covid-19. Imports dropped to 57,000 MT in July and further to 29,000 MT in August. As a consequence, in August, China’s year-to-date total imports was 2% behind 2019.

Figure 6: Year-to-date total growth rate 2019-2020 (including Ecuador supplies through Vietnam)

Source: Chinese customs

Figure 7: Volume (MT) of Chinese imports of warmwater shrimp (including Ecuador supplies through Vietnam)

Source: Chinese customs

The strict lockdown in China enabled the government to take control over the situation. Once under control, most of China was able to go back to normal life quite quickly. What I had not foreseen and what’s possibly a crucial factor in the drop of imports from July onwards is that seafood in general and shrimp in particular would become involved in Covid-19-related food scandals.

In July, after detecting traces of Covid-19 on the inside of a container with frozen shrimp from Ecuador, the Chinese government suddenly banned three Ecuadorian processors from shipping shrimp to China. Although this issue was generally quickly resolved, the impact on the market has been severe. Several Chinese retailers withdrew Ecuadorian products from their stores. Chinese buyers held their horses and did not place new orders in Ecuador. Luckily for Ecuador, after two months of no more positive tests, Undercurrent News reported that demand for Ecuadorian shrimp from China’s restaurants surged.

Although the first signs of an overall market recovery in China might be there, it’s still uncertain whether Chinese demand will strengthen towards the purchase season for Chinese New Year (12 February 2021). This will largely depend on whether more imported seafood will be tested positive for traces of Covid-19.

CONCLUSION

What will happen in the remainder of the year will depend to a large extent on how Covid-19 will continue to influence shrimp consumption around the world. In the EU and the US, restaurant sales will now really dwindle. It will probably only be after the first quarter of 2021 that restaurant sales start to turn back to normal levels. Until that time, retail will really have to keep the market afloat. In China, even though we might expect Chinese New Year to drive up the orders, it’s unclear to what extent consumption of imported shrimp will continue to be negatively affected by Covid-19 detections in frozen seafood imports. With so many uncertainties, it’s hard to predict in what direction the market will head. But if I were a shrimp farmer, I would be extremely cautious in planning my production for 2021 and try to look three to six months ahead, instead of focusing on the current – very changeable – situation.