I had initially planned to write one long blog in March discussing the latest data on production and exports in India, Indonesia and Vietnam. However, when writing my review and outlook for Indonesia, I realized that it was going to be a long one and that it simply would not do to keep you waiting. Therefore, I decided to break it up into several parts, of which you are currently reading the first one on Indonesia. Over the next couple of weeks, others will follow on India, Vietnam, and a final one with a more contextual discussion on the impact of the situation in those three countries on the global playing field, also looking at Ecuador’s performance in 2020 and the three main global shrimp markets – China, the EU and the US.

I’d like to offer a big thanks to my contacts at Indonesia’s shrimp feed manufacturers and shrimp processors and exporters for sharing their perspectives on the data I presented to them.

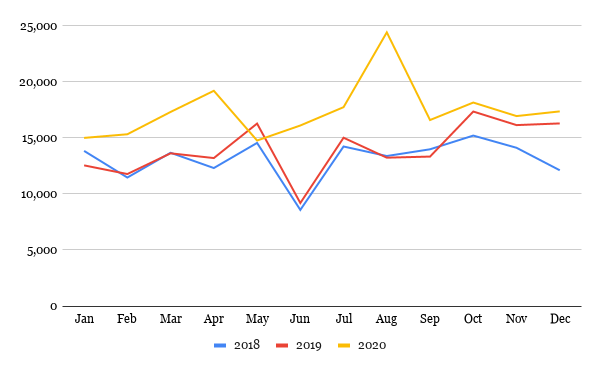

L. VANNAMEI VOLUME PRE-SHIPMENT TESTED INCREASED YEAR-ON-YEAR BY 24% TO 209,000 MT

In 2020, Indonesia showed the most impressive figures of all Asian producers. According to the department of the Ministry of Marine Affairs and Fisheries (MMAF) responsible for pre-shipment testing (BKIP), last year the volume of L. vannamei tested before shipment reached 209,000 MT. This is up 24% from 168,000 MT in 2019 and up 33% from 157,000 MT in 2018. Particularly from June till September, the volume was higher than previous years (Figure 1). Normally, the volume would drop after Ramadan and only show a moderate surge towards the end of the year. In 2020, the volume indeed dropped from April to May, but then rose rapidly every month to a peak of almost 25,000 MT in August, compared to 13,000 MT in 2018 and 2019 in that same month.

Figure 1: L. vannamei pre-shipment tested for exports

Source: BKIP, MMAF

Note: BKIP is responsible for pre-shipment testing. The data reported in their portal reflects the volume of L. vannamei shrimp that was pre-shipment tested. It does not state whether this product has actually been exported and there is a chance that some of the product is still in inventory in Indonesia.

One of my sources among Indonesia’s exporters mentions that another department of the MMAF, the Department for Competitiveness of Marine & Fisheries Production presented the actual export figures for 2020 in January of this year. The total shrimp export volume reached 239,000 MT, up 15% from 2019. L. vannamei accounted for 75% (180,000 MT), P. monodon for 16% and wild-caught shrimp for 9%. Putting the figures together, there’s a gap of almost 30,000 MT between the volume of L. vannamei that was pre-shipment tested and the volume that was actually exported. This product is most likely still in inventory in Indonesia. According to the same source, Indonesian exporters faced challenges in shipping their containers at the end of 2020. There was a shortage of cargo space on the container vessels and a lot of shipments were delayed from Q4 2020 to Q1 2021.

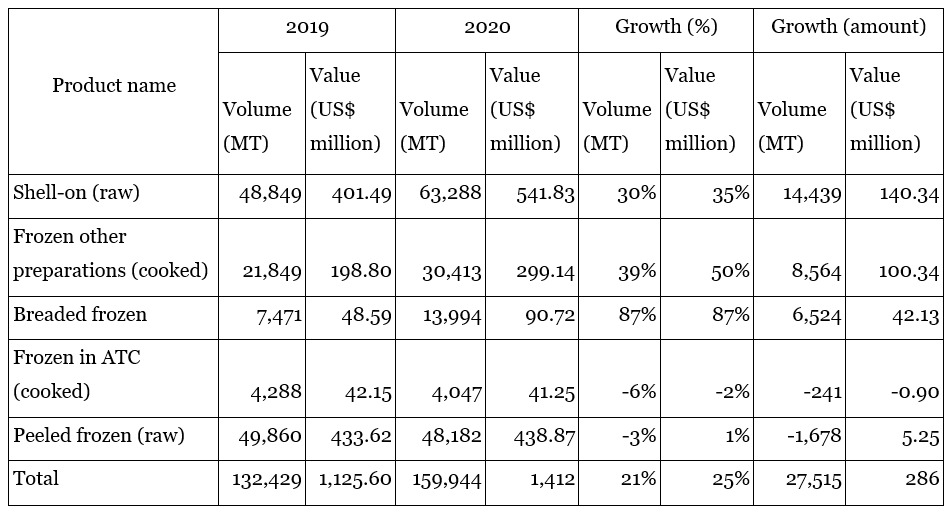

Unlike for instance Ecuador and India, Indonesia is not dependent on China for its exports. The US is Indonesia’s largest market and accounts for around 70-75% of L. vannamei exports alone. Japan accounts for about 15% and the remainder is scattered over China, the EU and other markets. The growth in Indonesia’s exports in 2020 was almost entirely caused by the US and the driving force in particular was increased demand from the retail segment, which was looking for other sources when Indian suppliers were not able to meet demand. The fact that retail was responsible for demand from Indonesia also shows from the type of products that were behind the growth (Table 1): headless shell-on (HLSO) (mainly easy peel (EZP)) (+30% or 14,000 MT), frozen cooked shrimp (+29% or 9,000 MT) and breaded shrimp (+87% or 7,000 MT). Within the HLSO (EZP) segment, the larger sizes such as <15 per kg (+84% or 3,000 MT), 15/20 per kg (+79% or 7,000 MT) and 21/25 per kg (+47% or 5,000 MT) mostly caused the growth, while the smaller sizes showed negative growth.

Table 1: US imports of Indonesian shrimp in 2019 and 2020

Source: NOAA

When I showed this breakdown of products imported from Indonesia to the US, one of the US importers involved in value-added products said he doesn’t think the surge of exports of breaded shrimp from Indonesia is due to an increase in total demand for breaded shrimp in the US but is rather due to US buyers shifting further away from China to Indonesia. He also mentions that with regard to raw material sourcing in Indonesia for value-added processing in the US, many buyers have moved away from Indonesia to e.g. Ecuador because Indonesian producers tend to focus more on larger sizes while these US buyers actually require smaller sizes. This is indeed reflected in the surge of exports of larger sizes HLSO (EZP).

THE INCREASE IN EXPORTS MIGHT NOT BE A RESULT OF A SIMILAR INCREASE OF PRODUCTION BUT OTHER FACTORS SUCH AS A DECLINE IN DOMESTIC CONSUMPTION MAY PLAY A ROLE

A big question for me is whether the increase in exports is a result of an increase in production or whether there are other factors at play. Not everyone in Indonesia seems to agree about this, but some of the data suggests it’s not necessarily due to an increase in production.

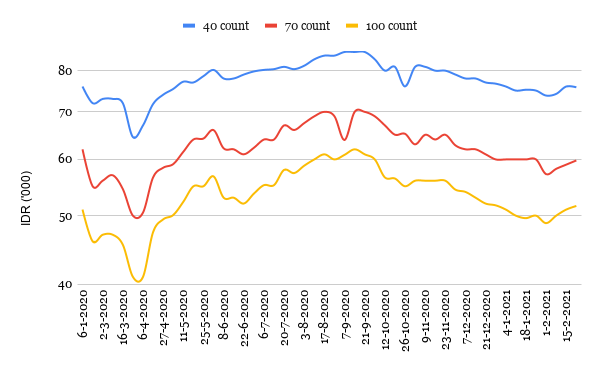

Most of my contacts at the feed companies and processors, based on a discussion of the export figures, gave me the impression that shrimp production in Indonesia was not severely impacted by the COVID-19 pandemic. According to them, while there were some disruptions in broodstock supplies and processing capacity from February till May, most farmers were able to continue production as usual. There was a slight scare in March when farmers were panic-selling their crops amidst restaurant closures overseas, and farm gate prices fell sharply as a result. But after that, driven by demand from the US, prices recovered (Figure 2). Although farmers struggled with disease, they managed to cope with the situation and harvested decent volumes. A possible explanation behind the sustained production volumes could be that many corporate farmers that, besides shrimp, normally also farm other proteins such as chicken and fish, had focused more on their shrimp in that period as that was the only product still in demand (i.e. due to demand from the export market).

Figure 2: Farm gate prices of Indonesian L. vannamei shrimp in 2020 and 2021 in East Java (Banyuwangi)

Source: Jala Tech

Another one of my contacts at a major feed manufacturer thought that production actually contracted in the range of 15-20%. A decline in domestic consumption would be responsible for the increase in exports. COVID-19 related restrictions have had a great impact on the food service market in Indonesia due to the closure of restaurants. As most shrimp is normally consumed in these restaurants, shrimp producers, according to this source, had to turn to the export market. Although I agree with my contact that Indonesia normally has a relatively high level of domestic shrimp consumption, at first I was hesitant to believe that this – i.e. the decrease of the domestic consumption – was the reason behind the increase in exports. To me, it is unclear to what extent domestic consumption is accounted for by L. vannamei or by wild-caught shrimp. An argument that I often hear is that L. vannamei shrimp is predominantly exported because it’s too expensive to compete with wild-caught shrimp and other proteins such as chicken and fish in the local market.

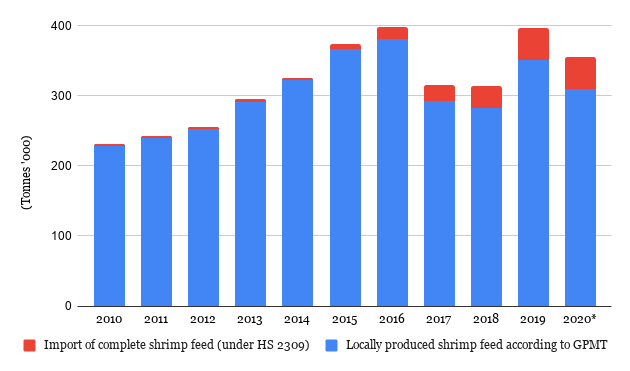

Luckily, I managed to get an idea of the amount of shrimp feed sold in 2020. Feed sales are normally a good indication of production. Although the Indonesian Feedmills Association (GPMT) has not yet officially published the figures for 2020, I obtained a preliminary figure from a local source of 309,000 MT of shrimp feed sold at the year-end of 2020 (Figure 3). If correct, this would constitute a decline of 12% compared to the amount of shrimp feed sold in 2019, which was just over 352,000 MT. We must keep in mind, though, that not all feed manufacturers are members of the GPMT. For example, a number of Chinese feed companies that opened facilities in Indonesia during the last couple of years are reportedly not yet a member of the GPMT but are likely to have taken some market share. Also, not all farmers use commercial shrimp feed and the volume of shrimp feed imported from China, Korea and Vietnam is increasing. Nevertheless, I do think that this number indicates that production of L. vannamei may have contracted and certainly did not increase as much as the exports did. A decline in domestic demand, combined with a strong US market, may indeed have played a role in the surge of exports.

Figure 2: Locally produced and imported shrimp feed from 2010-2020

Source: GPMT, Trademap and local sources in Indonesia

Note: The official data for domestic production for 2020 has not yet been released by the GPMT. The preliminary number is provided by a local industry source. The import numbers for 2020 have also not yet been published. In this figure, I assumed the volume of imported feed would be at least flat compared to 2019.

While the surge of farm gate prices between April and October was of course good news for the farmers, not all the players in the market benefited from this. According to one of my contacts at a major processor, exporters who are not vertically integrated into farming or feed have been struggling to make a profit as export prices didn’t increase as much as the farm gate prices. Nevertheless, these exporters had to continue exporting to repay their bank loans and because of retail contracts. Since prices came down in Q4 of 2020, and farm gate prices are now at par with those in India, exporters’ margins might improve, but my contact remains wary about the outlook for 2021.

HARVESTS FALL SHORT IN Q1 2020 DUE TO RAINY SEASON BUT OUTLOOK FOR THE SUMMER CROP OF 2021 SEEMS TO BE GOOD

Looking ahead to 2021, farmers have been experiencing challenges that may affect the harvest volume for the beginning of this year. According to one of the feed company representatives, problems occurred during the last stocking of 2020, which would be harvested during Q1 of 2021. Next to higher feed costs due to increased commodity prices, disease was rampant all over Indonesia due to the rainy season. Farmers reduced the number of ponds in operation and decreased stocking densities to cope with the situation. Besides some early harvests due to disease outbreaks, heavy rainfall caused floods in several locations such as Central Java, where farmers had to harvest their ponds to save their crops. As a result of these issues during the rainy season, the harvest volume during Q1 of 2021 is expected to be low. Whether it will be lower than other years remains to be seen as the rainy season crop is always the most challenging one of the year. So far, the shortage of raw materials has started to drive up farm gate prices, which is of course good news for the Indonesian shrimp farmers.

Photo 1: Intensive shrimp farm in Banyuwangi

Source: Larive International

The feed company representatives are more optimistic in terms of the first new stocking of 2021. Farmers were reportedly ready to stock as soon as the rain ceased, meaning that most likely many have started after mid-February, so harvests of this crop will likely outperform the pitiful harvest volume of the first crop of 2021. From an exporter’s point of view, however, the outlook for Q1 and Q2 is not good. Raw material prices are increasing and may only come down once the crop stocked in February is harvested, most likely from April till mid-May, just before Eid al-Fitr. With market prices not yet showing an improvement, freight costs still being at an extremely high level (mainly due to COVID-19), and the rupiah strengthening, packers are lucky if they can break even. According to one feed company representative, even though production may increase during the second half of 2021, due to the ongoing struggle with disease, it is uncertain whether production in 2021 will surpass last year’s record volume.

THE LONG-TERM OUTLOOK LOOKS PROMISING AND INDONESIA IS DEFINITELY ONE TO WATCH

In January, at the Indonesian Shrimp Forum, the MMAF provided some context to the 250% growth target which was announced by the Indonesian government last year. One of the Director Generals of the MMAF explains that by 2024 the government expects that the amount of intensive ponds will increase to 7,000 ha with a productivity of 40 MT/ha, amounting to 280,000 MT annually. In addition, the government expects semi-intensive production to increase to 30,000 ha with an average productivity of 8 MT/ha, amounting to 240,000 MT. Finally, extensive production in traditional ponds is expected to increase to 286,000 hectares with a productivity of 0.8 MT/ha, amounting to 228,000 MT. In theory, if these ambitions are met, production in Indonesia could surge to around 750,000 MT by 2024. The expansion of production is to be realized with the support of a set of interventions by the Indonesian government and industry, including (1) improved licensing for shrimp farms, (2) the prioritization of budgets allocated to shrimp farm expansion by the local and central governments, (3) the adoption of modern technology and supply of superior post-larvae and (4) the adoption of sustainable shrimp farming protocols as a prerequisite for licensing.

Most people are a bit skeptical about the reality behind the Indonesian government’s ambitious 250% growth target. I share this skepticism, especially bearing in mind that last year’s surge of exports may not entirely have been the result of an increase in production – which is exactly what is needed now to reach the target. However, together with industry leaders such as Grobest’s Samson Li and CPF’s Robins McIntosh, I do believe that Indonesia will likely increase its output over the next couple of years. Expansion of intensive and super-intensive shrimp farms will play a major role. But other developments such as the establishment of a local broodstock multiplication center by JAPFA and Kona Bay, and the market entry of American Penaeid Inc with its robust High Vigor broodstock, may also be important developments that will bolster the Indonesian industry’s growth. I expect that improved availability of consistently high-quality PL combined with more biosecure farms and sustainable production practices will result in an increase in Indonesian L. vannamei production in 2021 and beyond. As production expansion is likely to come not only from current production locations but also for a significant part from Eastern Indonesia and some parts of Sulawesi, an increase in production will need to be met with an expansion of processing infrastructure – a challenge for Eastern Indonesia in itself. Over the next couple of years, Indonesia will definitely be a country to watch.