In a previous blog, I provided a helicopter view of the shrimp importer landscape in the northwestern part of the EU. In this blog, I will explore the South of the EU market.

The South of the EU is the largest shrimp market in Europe. I define the region as (in order of largest shrimp markets) Spain, France, Italy, Portugal, and Greece. Each country has a rich seafood market, and shrimp imports have surged. The region, therefore, offers plenty of opportunities for shrimp exporters looking to grow their exports to the region.

I will start by discussing consumption, then dive into trade data, into the retail sector, and eventually provide a thorough overview of the leading importers and the key suppliers in the chilled and frozen segments.

In 2024, the Shrimp Blog is supported by: Inve Aquaculture, Taprobane Seafoods, DSM-Firmenich, Zeigler Nutrition, Bioiberica, Megasupply, American Penaeid, Omarsa and eFishery.

Shrimp consumption in the South of the EU

Unlike most of the rest of the EU, seafood consumption in Spain, France, Italy, Portugal, and Greece is deeply rooted in their culinary traditions and lifestyles. These countries record the EU’s highest consumption levels, from 61,5 kg per year in Portugal and 40 kg per year in Spain to 24 kg per year in France and Greece. Seafood is consumed throughout the year but with spikes during holidays and Catholic observances. Fresh seafood is preferred, although frozen and canned seafood are gaining popularity for convenience.

| Population size (million) | Seafood consumption per capita (kg/year) | Seafood market size (€bn) | Shrimp market size (€bn) | |

|---|---|---|---|---|

| Spain | 47 | 44 | 8-9 | 1.9 |

| France | 66 | 24 | 9 | 1.7 |

| Italy | 59 | 31 | 7-8 | 1.2 |

| Portugal | 10 | 62 | 2-3 | 0.4 |

| Greece | 10 | 24 | 1-1.5 | 0.3 |

Shrimp Trade in the South of the EU

This section will briefly describe the shrimp trade in the South of the EU. The analysis is limited to shrimp traded under HS030617 and HS160521/29. I will first provide some critical points for the region, then dive deeper into each country.

Regional Numbers

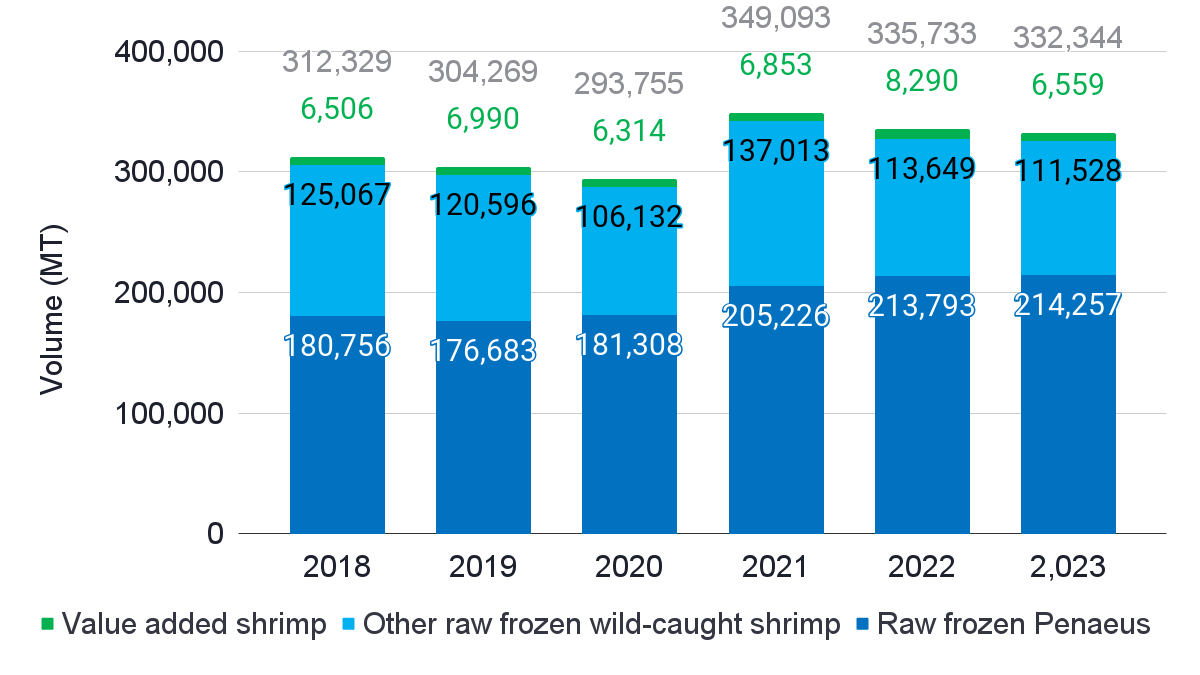

In 2023, the five countries in the South of the EU imported 332,000 MT of shrimp from outside the EU, down from a peak of 349,000 MT in 2021. Peneaus shrimp (HS03061792) represents 64% of the volume. Other species reported under HS03061799, including Argentinian red and Asian pink shrimp, account for 31%. Value-added shrimp represents only 3% of the volume. While imports of other wild-caught species under HS 03061799 declined since the peak in 2021, imports of Penaeus shrimp under HS 03061792 slightly increased.

Source: Eurostat

The five countries in the region also report importing 90,000 MT of shrimp from within the EU (both from within the South and from the Northwest of the EU). France represents 40% of those imports, Italy 22%, Spain 18%, Portugal 15%, and Greece 5%. While most intra-EU trade consists of raw frozen Penaeus and other species, 17% consists of value-added products, pointing to the EU’s reprocessing industry for refreshed and cooked shrimp. The countries also re-export some of the imported shrimp. Especially Spain is a significant re-exporter, supplying almost 40,000 MT to other EU member states. This confirms the role of Spain as a distributor of imported shrimp in the broader Southern EU region.

The table below summarizes the size of each market for these two product categories by looking at imports from outside the EU, imports from within the EU, and re-exports. The most important observation is that although Spain is the biggest importer of all species combined, France is the largest importer of Penaeus shrimp. If we include re-exports in the equation, domestic consumption of imported shrimp is not far apart between Spain and France.

| HS 03061792 (2023) | HS 03061799 (2023) | Total net imports | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Imports | Growth 2018-2023 | Exports | Net imports | Imports 2023 | Growth 2018-2023 | Exports | Net imports | ||

| Spain | 91,407 | 24% | 19,407 | 72,000 | 71,212 | -9% | 21,818 | 49,394 | 121,349 |

| France | 100,351 | 24% | 5,888 | 94,463 | 10,086 | -4% | 1,373 | 8,913 | 103,376 |

| Italy | 42,194 | 41% | 708 | 41,486 | 35,686 | -2% | 996 | 34,689 | 76,175 |

| Portugal | 13,669 | 16% | 1,767 | 11,902 | 10,713 | -26% | 4,262 | 6,451 | 20,120 |

| Greece | 8,133 | 118% | 765 | 7,368 | 7,088 | 107% | 1,640 | 5,488 | 12,856 |

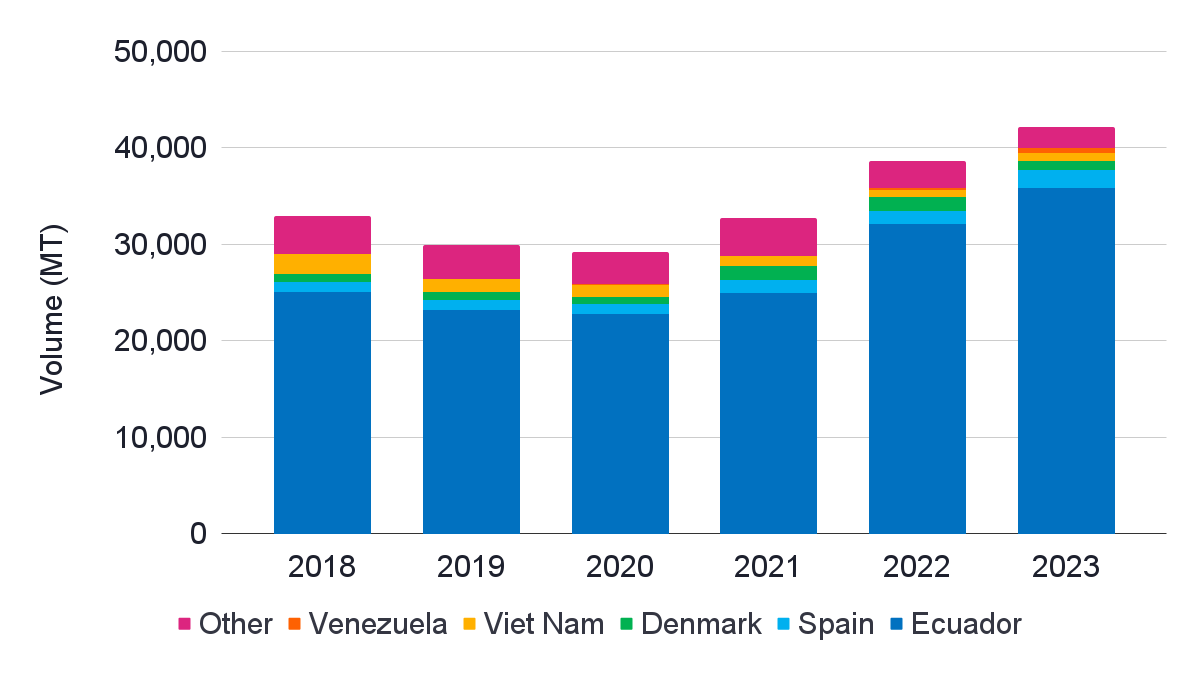

Spain

In 2023, 55% of Spain's imports consisted of Penaeus shrimp (of which 95% accounted for by L. vannamei), making Spain the region’s country least dominated by L. vannamei. Spain is also the largest importer of Argentinian red shrimp in the South of the EU. Argentinian red shrimp represents 30% of Spain’s imports. The remainder consists of Asian pink shrimp and shrimp from Africa.

Source: Eurostat

L. vannamei imports in Spain increased from 72,247 MT in 2018 to 89,286 MT in 2023, almost 20% growth. In 2023, Ecuador supplied 77% of the Penaeus shrimp and was responsible for most of the development of imports. Venezuela’s supplies doubled from 2018 to 2023, and it has now become the second largest supplier, although it still represents only 9% of total imports. Other smaller suppliers include Nicaragua, Peru, and Colombia. The Netherlands complements the top five as it has quadrupled its supplies to Spain, most likely primarily of peeled products.

With nearly 20,000 MT, Spain is also a significant exporter of raw frozen Penaeus shrimp, primarily exporting to its neighboring countries, Portugal, France, and Italy. It also exports substantial amounts of Argentinian red shrimp to neighboring countries. As such, Spain is a regional trading hub like the Netherlands and Belgium in the Northwestern part of the EU.

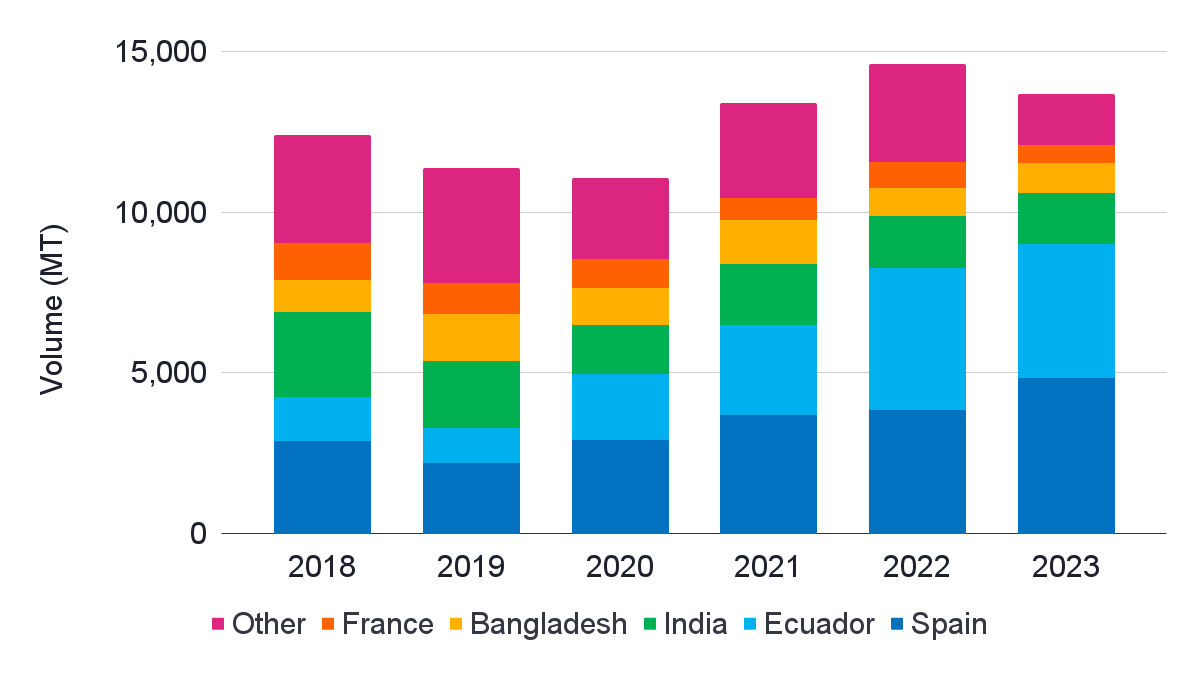

France

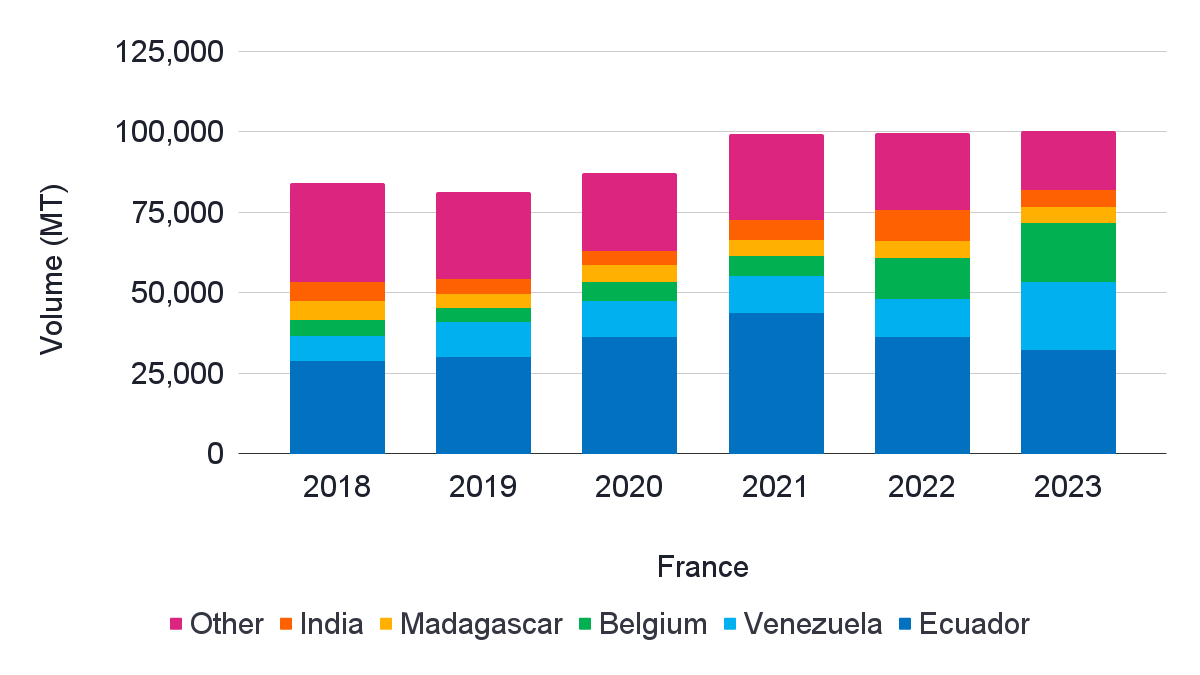

Penaeus shrimp imports in France represent 81% of total shrimp imports (of which roughly 90% is accounted for by L. vannamei). The country also imports 9% of value-added products, the highest in the region. Other wild-caught species don’t play a decisive role in the market. Still, shrimp from Africa (primarily Madagascar) have a special place due to historical ties and investments in shrimp fisheries and farming operations.

Source: Eurostat

Penaeus shrimp imports in France increased from 84,217 MT in 2018 to 99,506 MT in 2023, a 15% growth. However, growth has stagnated since 2021. Ecuador increased its supplies to France by 12% from 2018 to 2023, which is not the significant growth we saw in Spain. With 32%, Ecuador is also a less dominant supplier compared to its position in Spain. Venezuela grew significantly as it almost tripled its supplies and consolidated its position as the second largest supplier (21% market share), encroaching on Ecuador rapidly. India looked like growing its exports, doubling supplies from 2019 to 2022, but then supplies dropped back in 2023. Vietnam and Bangladesh saw supplies fall. Madagascar maintains stable supplies to France and remains the country’s largest P. monodon supplier, though just at a volume of around 5,000 MT annually.

From within the EU, Belgium is France’s largest supplier of Penaeus shrimp, mainly because some of the importers in Northern France use the port of Antwerp as a point of entry for the French market.

Italy

Penaeus shrimp imports in Italy represent just 48% of total imports in 2023 (of which L. vannamei accounts for 95%). Like in Spain, Argentinian red shrimp plays an important role and represents almost 30% of total imports.

Source: Eurostat

After a long period of market stagnation, Italy’s Penaeus imports grew in 2021 and surpassed 40,000 MT in 2023. Ecuador accounts for 85% of the total supplies from outside the EU and is by far Ecuador’s largest supplier of Penaeus shrimp. Other imports from outside the EU come from Vietnam (falling), Venezuela (increasing), and India (falling).

Spain is Italy’s second-largest supplier, but it has a market share of only 5%. Denmark and the Netherlands also supply small volumes, most likely mainly peeled products.

Portugal

In 2023, raw Panaeus imports represented 50% of total shrimp imports in Portugal. The rest of the market consists of a mix of Argentinian red shrimp (supplied through Spain), Asian pink shrimp (from India and China), and African wild-caught shrimp (mainly from Mozambique–a premium product in the Portuguese market).

Source: Eurostat

Raw Panaeus imports grew from 12,411 MT in 2018 to 14,615 MT in 2022 and dropped back to 13,669 MT in 2023. Most of Portugal’s Penaeus imports are sourced from within the EU, with Spain being the largest supplier and France being the fifth largest supplier. That said, Ecuador has been rapidly increasing its direct exports to Portugal and, in 2023, even surpassed Spain as the number one supplier. Bangladesh and India also supply P. monodon to the Portuguese market.

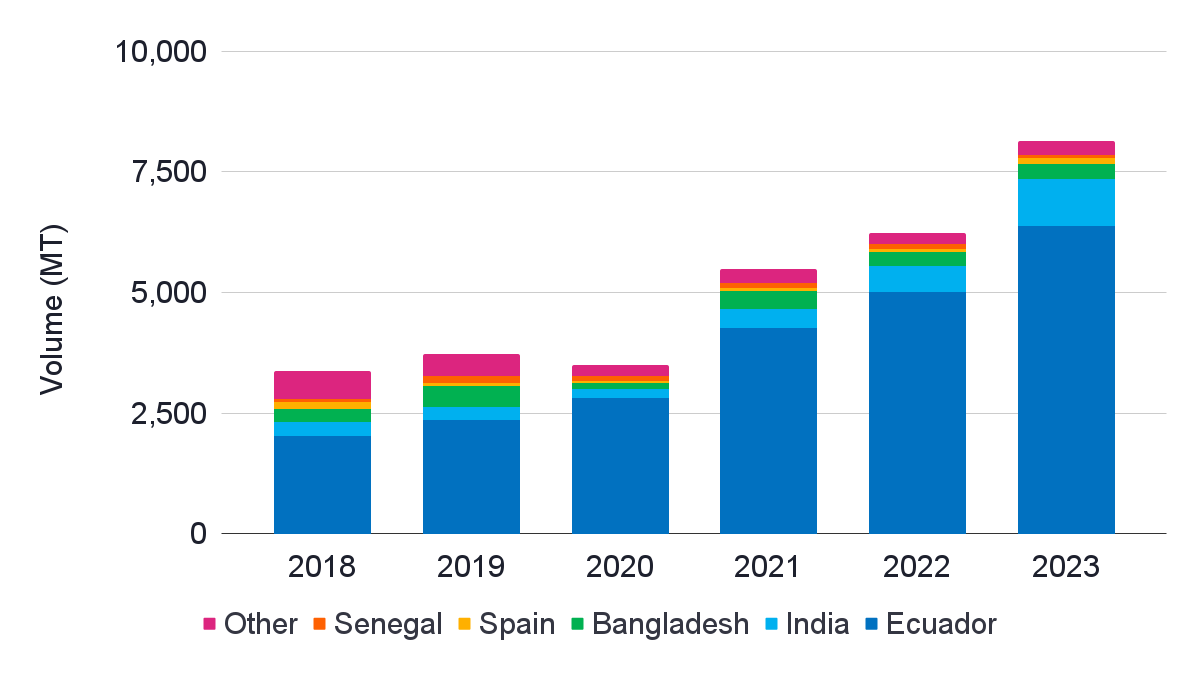

Greece

In 2023, 50% of Greece's imports consisted of raw Panaeus shrimp. Asian wild-caught pink shrimp and a range of other species comprise the remainder. While just over 8,000 MT is still the region’s smallest market, its raw Panaeus imports are growing fast, having more than doubled since 2018.

Source: Eurostat

Ecuador supplies 78% of Greece’s raw Penaeus shrimp imports, and Greece is one of the markets in which Ecuador aims to diversify its export destinations. India (in 2023, responsible for 12% of Penaeus imports) has also been growing supplies to the market.

Asian pink shrimp is primarily sourced from India, partly through the Netherlands and Germany. Argentinian red shrimp is imported directly from Argentina and Spain.

The Retail Market in the South of the EU

The countries in the South of the EU have an out-of-home dinner culture and a large Horeca sector catering to the local population and the many tourists that visit the region, especially on the coast and on the many islands. Large broad-line food wholesalers and specialized seafood wholesalers supply the HORECA sector. Nevertheless, most seafood is sold through retail. Modern super and hypermarkets are the most substantial retail sales channels, but traditional fishmongers also continue to play an important role, especially in Greece and Portugal. While the HORECA sector is highly fragmented, the supermarket channel is relatively consolidated, with a few players dominating the market in each country. These retailers are responsible for the most significant volumes of shrimp sales.

| Share of retail in seafood sales (%) | Share of super and hypermarkets in retail seafood sales (%) | |

|---|---|---|

| France | 65 | 80 |

| Italy | 60 | 70 |

| Spain | 70 | 75 |

| Portugal | 65 | 65 |

| Greece | 55 | 65 |

Food Retailers in the South of the EU

As most of the imported shrimp is sold through the retail channel, in this section, I will dive a bit deeper into which retail chains dominate the market in the South of the EU. I have asked ChatGPT to help me with some numbers (of course, cross-referencing for accuracy). According to ChatGPT, the total food market size in the religion is €578bn. The largest market in terms of food retail market size is France (€255bn), followed by Italy (€162bn), Spain (€115bn), Portugal (€25bn) and Greece (€21bn). The following section will review each country's top five retailers.

Spain

In Spain, supermarkets sell most shrimp products in bulk, chilled and cooked in the fresh counter. Retailers offer a mix of private label and branded products in the small prepacked fresh and frozen sections. The five most prominent chains in Spain's grocery retail sector—Mercadona, Carrefour, Lidl, Eroski, and DIA—control over half of the market.

- Mercadona is the clear leader, with an approximately 26.8% market share in 2024. Mercadona is locally owned and not part of a larger international group. In Spain, the company operates around 1,600 stores.

- France’s Carrefour has a 10% market share. Groups such as Mercadona, Lidl, and Aldi continue to pressure it. The company has around 1,900 stores across the country.

- El Corte Ingles has around 7% of Spain’s grocery market, though its share is more significant in non-food items than food items. For its food sales, the group owns 90 super and hypermarkets. It is a locally owned retailer with a relatively stable market share.

- Lidl secures fourth place with 6.6%. Spain is an essential country for Germany's Schwarz Gruppe, to which Lidl belongs, and its market share has gradually grown. Today, the group has around 600 stores nationwide.

- Eroski holds 4.2% and is gradually growing its business by opening new stores through its franchise model. The group is dominant in Basque and owns around 1,087 stores nationwide.

German discounter Aldi has a small market share in Spain, around 2%. However, the company is expanding rapidly, opening 50 stores in 2023 alone. Auchan is also active in Spain under the banner of Alcampo. It has a market share of almost 4%.

Mercadona’s New Fish Model

Source: Mercadona Webshop

To combat the drop in fish consumption in Spain (which dropped from above 27 kg yearly in 2013 to just 18 in 2023), Mercadona started a pilot in 2024 to revamp the way it sells fish and seafood to its customers. This concept is tested in 100 of its 1,600 stores and will be scaled if successful. If indeed successful, it could fundamentally change how shrimp is sold in Spain’s supermarkets, getting it closer to how supermarkets in France and Northern European countries offer shrimp, where many more items (especially peeled) are already pre-packed on trays.

At Mercadona, there was already a difference in the color of the large trays in which seafood was sold in its supermarkets–blue trays for wild seafood and green for farmed seafood. In this way, consumers can easily distinguish the two origins. However, Mercadona presents its fresh seafood to its customers in a more revolutionary way. In Spain, seafood has always been sold in bulk and prepared and packed for the customer on the spot by the supermarket’s fishmonger. Mercadona is now testing whether sales increase if more seafood items are prepacked on trays and presented on shelves, just like in the supermarket's meat section, where much of the products are already pre-packed.

The small trays are made from 100% recyclable plastic. Products are cleaned and ready to cook. In the case of shrimp, a mix of head-on and peeled products is available. This new model should reduce the waiting time in the store, reduce waste, possibly reduce prices, and reduce preparation times at home. Another advantage for the customer is the longer shelf life of prepacked trays, up to 6 days. According to the retailer's CEO, self-service and a more convenient shopping and cooking experience should hopefully increase the sales volume, reducing or even turning around the negative trend of dropping fresh seafood consumption.

France

According to ChatGPT, the five most prominent chains in France’s grocery retail sector– E.Leclerc, Carrefour, Les Mousquetaires (Intermache & Netto), Systeme U, and Auchan control around 80% of the market. As such, the French retail market is much more consolidated than the market in Spain. Some of these groups are among Europe’s largest retailers, having stores in many European countries and other parts of the world.

- E.Leclerc is the clear leader, with an approximate 24% market share in 2024. It’s a cooperative supermarket owned by store owners that operates under its banners. It has close to 1,000 stores across the country. The company is not very active outside France.

- Carrefour has a market share of around 21% and is a market leader in other countries besides France, such as Spain, Italy, and Belgium. The company owns 5,800 supermarkets, hypermarkets, and convenience stores in France. Surprisingly, the owners of Auchan, one of its competitors, are also shareholders in Carrefour.

- Les Mousquetaires, which operates stores under the Intermarché and Netto brands, has a 15% market share and operates around 2,200 stores nationwide. The group is also active in Belgium, Poland, and Portugal, among other places. It’s one of Europe’s largest retail groups.

- Système U is a cooperative-based retail group with a 12% market share. It’s locally owned and does not have many activities outside of France. In France, it operates close to 1,000 stores.

- Like the others, Auchan is French-owned, has an 8% market share, and operates around 2,000 stores nationwide. The group's family also owns other chains, such as Decathlon, the European market leader in outdoor gear. While active in Spain, Portugal, and Poland, Auchan has exited countries such as China and Vietnam.

Germany’s Lidl and Aldi also have notable shares, with Lidl holding around 7.5% and Aldi at 3.3%. The French market is highly competitive, with discounters like Lidl and Aldi continuing to expand their presence.

French supermarkets sell around 40,000 MT of chilled and cooked shrimp in French Supermarkets.

Agrimer’s annual consumer seafood survey suggests that in 2023, French supermarkets sold almost 40,000 MT of chilled and cooked shrimp, valued at nearly €600m. Of the total amount, 55% would be sold from products without bar code (bulk in fresh counter), and 45% would be sold with barcode (prepacked). However, sales of products with bar codes generate more value, representing 52% of the value. 48% of households buy shrimp with a bar code at least once a year. 42% of households purchase shrimp without a bar code at least once a year. Sales of frozen shrimp in retail are negligible compared to the sales of chilled cooked shrimp.

Regarding sales of shellfish and crustaceans in the food service segment, more than 90% are sold through independent restaurants and restaurant chains; sales to institutional food service are negligible due to the relatively high price of these products. Generally speaking, across products, individual restaurants buy 76% of fish and seafood as fresh or chilled products, 21% as frozen products, and the remainder canned. Restaurant chains buy 50% frozen, 49% fresh or chilled, and the remainder canned.

Italy

Italy's top five grocery retail chains are Coop Italy, Conad, Esselunga, Selex, and Lidl. Combined, the top five have a market share of around 54%, a similar level of consolidation to that seen in Spain.

- Coop Italia is Italy’s market leader; different sources mention 14% to 21% market shares. The chain has a strong nationwide presence with more than 1,000 stores.

- Selex is an alliance of regional retailers under the Selex brand. It focuses on proximity shopping and affordability. The company has a 13-14% market share and operates over 2,000 stores nationwide.

- Conad is another cooperative supermarket chain with a smaller market share of 13-14%. Like Coop, it has a wide presence nationwide and a strong focus on sustainability. It operates 3,500 supermarkets, hypermarkets, and smaller stores across the country.

- Esselunga is dominant in northern Italy and is often perceived as a premium supermarket chain. It has around 9% market share and operates 191 supermarkets.

- Lidl is rapidly growing its market share in Italy, benefiting from the rising popularity of discount stores. It has 700 stores already and plans to open another 150 in 2024. In 2023, its market share was 9%.

Other international retailers, such as Carrefour Italy and Aldi, are also active in Italy, with a market share of around 8%. Once a significant retailer in Italy under its Alcampo brand, Auchan sold most of its stores to Conad and Coop Italy and is now a minor player.

Portugal

The top retailers in Portugal are Continente, Ping Doce, Lidl, Intermarche, Auchan, and Miniprecio. Most of these chains are part of larger international retail groups rather than locally owned. The top five combined have approximately 80% market share, so the market is highly consolidated.

- Continente is Portugal’s largest retail chain, with over 700 stores nationwide and an approximately 27% share. It’s the only significant retailer not part of a larger international group. The company is owned by Sonae, one of Portugal’s largest multinationals.

- Pingo Doce, a JV between Portugal’s Jeronimo Martin’s (51%) and the Netherlands-based Ahold Delhaize (49%). The company operates around 400 stores nationwide, holding the second-largest share at 23%.

- Lidl rapidly expands in Portugal, operates 271 stores, and holds a 13-14% market share.

- Intermarché, part of the French retail group Les Mousquetaires, has a 9% market share and operates over 250 supermarkets nationwide. The company’s market share has increased over the past few years.

- Auchan (Jumbo), another French-based retail group, has a steady market share of around 7%. In Portugal, Auchan operates through a combination of hypermarkets and convenience stores. After acquiring 489 Minipreço and Mais Perto stores (formerly owned by Dia), Auchan significantly expanded its footprint. This acquisition added to its existing network of over 100 stores,

Chains like Aldi (5% market share) and Mercadona (3% market share) are also gaining traction in Portugal. Mercadona, for instance, has significantly increased its footprint since entering the Portuguese market in 2019 and is expected to open 11 more stores in 2024

Greece

In Greece, the grocery retail market is led by several major players, including Sklavenitis Group, AB Vasilopoulos, Lidl Hellas, Metro Aebe, and Masoutis.

- Sklavenitis Group is the largest retailer, with a significant market share driven by its 438 outlets and annual turnover exceeding €4 billion in 2022. The group is not part of a larger multinational retail group. Its market share is unknown but believed to be around 20-25%. The company also bought Metro Germany’s Makro wholesale stores in the country.

- AB Vasilopoulos (Ahold Delhaize group) is a strong competitor. As of 2023, it had a turnover of €1.92 billion and a network of 582 stores. Its market share is believed to be around 13-14%. The group also has a smaller wholesale business through some of its formats.

- Lidl Hellas, part of the Schwarz Group, operates 235 stores and reported a turnover of €1.8 billion. Its market share is unknown but estimated at around 15-20%. The company has announced that it will invest €120 million in existing and new operations in the country between 2024 and 2026.

- Metro Aebe, managing My Market and Metro Cash & Carry, achieved €1.48 billion turnover, with a mix of retail and wholesale operations. Although it shares the name with the German Metro Group, Metro Aebe is an independent Greek-owned company. Its exact market share is unknown but estimated to be around 10%.

- Masoutis, a leader in Northern Greece, posted a turnover of €935 million across its 387 stores. It has a market share of around 10% and is expanding its presence nationwide.

Smaller chains such as Galaxias, Market In, and Synka contribute to the competitive landscape but have under €514 million in turnover. Other international retail chains such as Aldi, Auchan, and Carrefour only have minor market shares in Greece.

The Importer Landscape

Like in Northwestern Europe, three main categories of importers supply three distinct market segments in the South of the EU.

- The first group is the reprocessors, the cookers. These import bulk, reprocess it within the EU, and distribute it as refreshed products directly to supermarkets, wholesalers, and industry. This group is consolidated. Although smaller players exist, typically, reprocessors are large companies with significant investments in infrastructure and logistics and substantial financial means to manage working capital requirements. While most reprocessors are importers and distributors, some only operate as service providers. These are less visible in the market and are not covered in this blog.

- The second group is the suppliers of frozen shrimp to supermarkets. Although these companies require less infrastructure, they need the financial strength to handle stocks required for large retail contracts. This relatively small group overlaps with the first and second groups, as most suppliers of chilled cooked products are also active in the frozen segment and have a wide range of frozen products in their portfolio.

- The third group consists of companies that predominantly supply the large but fragmented wholesale sector. These companies are often smaller, operate more locally, and purchase shrimp mostly on a spot market rather than on a contract basis. While the first two groups are typically also active in this third segment, this third group of companies is usually not active in the supermarket segment.

The chilled and cooked shrimp market

Most shrimp in supermarkets in Spain and France are sold as freshly cooked head-on on a fresh counter. Most retailers also offer a range of refreshed, cooked, peeled items. While companies within the region produce most cooked head-on products, the peeled products are often supplied by companies such as Heiploeg and Klaas Puul in the Northwestern part of the EU, which specialize in those products. This section will only present the major cookeries from Spain and France. While smaller cookers may exist in Italy, Greece, and Portugal, the chilled segment is less important in these countries, and companies like Pescanova and Profand supply most chilled and cooked shrimp.

Spain

Spain is home to the region’s biggest cookers. At least 10-15 companies supply chilled and cooked products to the market, but three to five companies dominate the retail sector. This section covers the most well-known cookers, big and small.

Nueva Pescanova

Founded: 1960

Country: Spain

Estimated turnover in 2023: €970m

Owned by: Irrelevant

Relevant group companies: Promarisco (Ecuador), Camanica (Nicaragua), Abad Overseas (India), Argenova (Argentina), Pescanova Hellas, Pescanova France, Pescanova Spain, Pescanova USA.

Pescanova is Europe’s largest shrimp trading company. The group sources shrimp primarily from its operations in Argentina, Ecuador, Nicaragua, and Guatemala. The farming operation covers 7,000 ha and is concentrated in Ecuador and Nicaragua. The processing plants in Ecuador and Nicaragua primarily produce head-on shell-on products. The Guatemala plant is the production hub for the company’s peeled and value-added products.

The group processes around 60,000 MT of shrimp annually. Most of its product is sourced raw head-on and supplied to its shrimp processing plants in Spain and France. Its two cookeries in Spain can cook around 26,000 MT annually, and its cookeries in France can process around 25,000 MT annually. From these plants, it supplies shrimp across the region. The company also packs frozen shrimp as a final product in Latin America. With its refreshed and frozen product range, the company has a presence in almost every of the region’s supermarket chains. If not with shrimp, then with its range of fish products.

The company reported substantial financial losses in its last fiscal year. Attempts to sell the company or parts of it have been made, but these efforts have failed.

Grupo Profand

Founded: 1986

Country: Spain

Estimated turnover in 2023: €930m

Relevant group companies: Profand Spain, Cocedero de Mariscos (Spain), Consermar (Argentina), Profand Ecuador, Stavis Seafood (USA)

Profand is a fishing company at heart but has also invested in aquaculture operations. It has been making several acquisitions in aquaculture production and seafood distribution since 2021, when it signed a €100m investment from a Spanish investment fund in exchange for 24% of the company’s shares. Regarding aquaculture, it first invested in seabass and seabream through Kefalonia Fisheries and, more recently, in Profand Ecuador, which it says is an aquaculture project. Regarding its investment in Ecuador, as UndercurrentNews reported, the company bought a small shrimp farm (300 ha) and was co-packing at a company called Vannapack at the time of the report. The article argued that Profand might be eyeing acquiring Vannapack or its sister company, Winrep.

Eyeing aggressive expansion in Spain’s shrimp market, in 2019, Profand acquired Cocedero de Mariscos (also known as Caladero), Mercadona’s seafood distribution company, and became Mercadona’s largest shrimp supplier immediately. Caladero, at that time, could cook 20,000 MT of shrimp annually. It’s unclear how large Profand’s total shrimp processing capacity is today, but it’s clear that Profand has become Nueva Pescanova’s biggest competitor in the retail market, offering its customers a wide range of Argentinian red and vannamei shrimp. Profand is also eyeing expansion in France and other markets in the region. The group acquired Stavis Seafoods and two other seafood distributors in the US to extend its reach in the North American market.

Angulas Aguinaga

Founded: 1974

Country: Spain

Estimated turnover in 2023: €250-300

Owned by: Pai Partners and Portobello Capital

Angulas Aguinaga is a prominent Spanish food company specializing in seafood products, particularly refrigerated and ready-to-eat segments; shrimp is just a tiny part of its product portfolio. Known for its innovation, the company markets popular brands like La Gula del Norte and Aguinamar. Angulas Aguinaga has been significantly expanding its international footprint, with a presence in 24 countries. It operates seven production plants, including two in Italy. The company is partially owned by private equity firm PAI Partners, which acquired a majority stake in 2020, while Portobello Capital and the founding family retained a combined 49.9% ownership. Its shrimp range mainly consists of marinated skewers and cooked and marinated shrimp tails, sold under its Aguinamar brands. Sales enter the wholesale and food service segment, but also increasingly the retail segment. It sources shrimp directly from overseas suppliers and sources from other companies within the EU.

Gambastar

Gambastar

Founded: 2003

Country: Spain

Estimated turnover in 2023: €75-100m

Owned by: Primstar

Relevant group companies: Atlantic Shrimpers, Primstar, Cornelis Vrolijk

Gambastar is another of Spain’s top three shrimp processors. At its production site in Burgos, Spain, it can cook around 10,000 MT of shrimp yearly. As such, Gambastar is a small player compared to Nueva Pescanova but has a solid position in the Spanish market. While most of its business consists of cooked head-on, which it imports in bulk, it also offers a range of frozen products in several major supermarket chains in Spain.

The company is less active in other parts of the region than Nueva Pescanova. That said, it has sales agents in France, Italy, and Portugal. The company is owned by Primstar, which is based in the Netherlands and owned by Dutch fishing giant Cornelis Vrolijk. Primstar invests in shrimp farming and fishing in Ecuador and Nigeria. Philippe Guiard, a veteran buyer from the industry, currently leads Gambastar.

Pescafacil

Founded: 1993

Country: Spain

Estimated turnover in 2023: €25-50m

Owned by: Lamar Group (Venezuela)

Relevant group companies: Lamar Group

Pescafacil operates out of Burgos, Spain. A former employee of Pescanova started the company; today, it is run by his sons. In 1997, Pescafacil started cooking shrimp. In 2018, the company merged in a strategic alliance with Lamar Group from Venezuela, after which several investments in its processing plant followed. Today, Pescafacil is processing and distributing Lamar’s shrimp across the South of the EU, especially in Spain. While part of Grupo Lamar, Pescafacil imports shrimp from other origins, especially Ecuador. The estimated volume of products imported from Venezuela is 5,000 to 7,500 MT. Besides shrimp, the company also offers various seafood products, including octopus.

Congelados Apolo

Founded: 1963

Country: Spain

Estimated turnover in 2023: €50-60m

Congelados Apolo is a seafood wholesaler specializing in frozen and cooked products. It has cooking lines for shrimp and Octopus. It is estimated to distribute at least 1,500 MT of cooked farmed shrimp annually—a small but specialized and well-respected player in the wholesale market.

Jaime Soriano

Founded:

Country: Spain

Estimated turnover in 2023: €40-50m

Owned by: D’Agustin

D’Agustin is a significant shrimp group from Central America. In 2021, the company reported financial revenues of €10-12m from its farming and processing operations in Honduras and Nicaragua. In Spain, Jaime Soriano reported revenues of $42m, with additional sales revenues of €23m from VentaPesca, another group subsidiary. Jaime Soriano imports not only from Honduras and Nicaragua but also from Ecuador and possibly other countries.

Compesca

Founded: 1970

Country: Spain

Estimated turnover in 2023: €25-50m

Compesca is a smaller seafood processor with the capacity to cook shrimp. The company imports from Latin America and supplies mainly to the wholesale market. The company claims its 10-day shelf life for its cooked shrimp as its main USP compared to other cookers.

Mariscos Castellar

Founded: 2015

Country: Spain

Estimated turnover in 2023: €40-45m

Castellar, located close to Barcelona, mainly supplies the HORECA market in the region with a range of chilled, cooked, and frozen L. vannamei, local wild-caught shrimp, and other seafood products such as crab and langoustines. In ten years, the family that owns the company has grown the business to around €35m in sales in 2023.

Langus Seafood SL

Founded: 2008

Country: Spain

Estimated turnover in 2023: €20-30m

The company's owners founded Ultracongelados Antartida in 1989. This company grew into Spain’s largest shrimp cooker, with a market share of around 60% in 2000. In 2002, when the factory had a capacity of around 25,000 MT per year, the company’s facility was sold to Nueva Pescanova. In 2005, the company’s owners started a new shrimp cooking project with Angulas Aguinaga, and in 2008, Langus Seafood was established. Today, the company sources shrimp from Latin America, cooks and packs it in its facility in Burgos, and sells it to the wholesale and retail market, intending to offer a premium, high-quality product.

France

The cooking sector in France is even more consolidated than in Spain. Larger food groups or seafood companies have acquired most cookers, but a few smaller independent cookers are still available. The larger cookers are Labeyrie Fine Foods (Delpierre), Nueva Pescanova (not separately discussed here), Capitaine Houat (Les Mousquetieres), and Crusta C (Groupe JMI). Smaller cookers include Unima, Senacrus (Captain Fresh), L’assiette bleue (Escal), and Cite Marine (Nissui).

Delpierre

Founded: 1913

Country: France

Estimated turnover in 2023: $300-400m

Owned by: Labeyrie Fine Foods

Relevant group companies: Lyons Seafood

Delpierre, as part of Labeyrie Frozen Foods, dominates the French shrimp market, supplying large volumes of chilled and cooked unbranded bulk products and chilled and cooked packaged products under its brand. 100% of Delpierre’s farmed shrimp supply is certified by ASC. The company has four seafood processing sites, one of which is set up for shrimp. Delpierre (also known as Adrimex) became part of Labeyrie Fine Foods in 2007. In 2004, Lyons Seafood was added to the Labeyrie group. With Delpierre and Lyons, Labeyrie Fine Foods claims to be the number one player in the French and UK shrimp market.

Crusta C

Founded: 1993

Country: France

Estimated turnover in 2023: $120-150m

Owned by: Groupe JMI

Relevant group companies: Gelpeche (France), Nov’East Seafood (Romania), Refripeche (Madagascar)

The company was established as Crusta d’Oc in 1993. Since then, it has opened three more processing facilities, which have allowed it to sell shrimp nationwide. While the first three facilities catered mainly to the Horeca segment, the last establishment opened in 2020 and was designed to cater to supermarkets. The site is fully automated and ASC-certified. Although official figures are unavailable, on its website, the company reports that it has sold more than 15,000 MT of shrimp and reached a turnover of €120m in 2019.

The company joined Groupe JMI in 2017. Today, JMI is one of the most prominent shrimp groups in the South of the EU. Groupe JMI comprises a range of companies invested in shrimp farming in Ecuador (3,500 MT), trout farming in France (1,200 MT), fishing companies in Madagascar (1,250 MT of wild-caught prawn), shrimp cooking facilities in France and Romania, a wholesale company in France, and a specialized frozen seafood company (Gelpeche) in France.

Capitaine Houat

Founded: 1988

Country: France

Estimated turnover in 2023: €300-350m

Owned by: Les Mousquetaires (Intermarche)

Capitaine Houat is owned by Les Mousquetaires, to which Intermarche, one of France’s largest retailers, belongs. The company has several processing sites across France and processes practically all private-label seafood for the group’s supermarket chains. The group has been facing financial headwinds recently, reporting losses for several years and announcing restructuring plans in 2024. The group is believed to process around 40,000 MT of seafood annually, of which the majority comprises fish fillets. Shrimp cooking is also a significant part of its activities. It’s one of France’s largest seafood companies.

Cite Marine

Founded: 1990

Country: France

Estimated turnover in 2023: €75-100m

Owned by: Nissui

Relevant group companies: Sealord (New Sealand), Nordic Seafood (Denmark), J. P. Klausen (Germany)

In 2019, Cite Marine acquired Miti, the value-added shrimp division of Le Mousquetaires Group. Miti offers a range of ready-to-cook and ready-to-eat shrimp products, including tapas and breaded shrimp. In 2024, the group acquired another French tapas producer who operates under Cite Marine's wings and sells products under the Miti brand. Since 2009, Cite Marine has been part of Japanese seafood giant Nissui, connecting it to Nissui’s network of seafood trading and value-added processing subsidiaries worldwide. Its value-added shrimp items are found in many supermarket chains in France.

L’Assiette Bleue

Founded: 1997

Country: France

Estimated turnover in 2023: €15-30m

Owned by: Escal

This is a relatively small value-added seafood producer. It offers natural shrimp products without conservatives. All shrimp items are certified by ASC or organic. These products are available in most of France’s major supermarkets. In 2020, the company was acquired by French frozen seafood importer and distributor Escal. For Escal, the acquisition of the company ment its entry into the chilled cooked segment of the French seafood market.

Unima Fresh

Founded: 1965

Country: France

Estimated turnover in 2023: Unknown

Unima Group is the most prominent shrimp farmer in Madagascar and runs a distribution business in France. It started fishing shrimp in Madagascar in the 1970s and, in the 1990s, ventured into shrimp farming. It has its cookery and distribution facilities in France. Its farmed shrimp was the first non-European food product permitted to join Label Rouge, a label for premium food products in the French market. Its farm was also the first aquaculture operation in Africa to receive ASC certification in 2016. Its shrimp are sold in most of France’s major retail chains as premium options within the shrimp category.

Senecrus

Founded:

Country: France

Estimated turnover in 2023: €20-25m

Owned by: Captain Fresh (India)

Relevant group companies: Censea (USA)

Senecrus is a smaller chilled and cooked shrimp producer in France, which in 2023 was acquired by Indian start-up Captain Fresh. Captain Fresh aims to build a global platform for selling and distributing seafood. Besides Senacrus in France, it acquired a salmon smoker in Poland and Censea, a major US shrimp importer and distributor. More acquisitions from Captain Fresh are to be expected. Captain Fresh has filed for IPO at the stock exchange in India and is expected to list in 2025 or early 2026.

Suppliers of Frozen Shrimp

Spain

The frozen shrimp market in Spain is less prominent than the chilled and cooked market. Nevertheless, most cookers also have a frozen product range. Although there are many importers of frozen products, most are small. Here, we only add Pescatrade to the list as its products are in several retail chains. Other smaller-volume importers include Roda International and Golden Mar.

Pescatrade

Founded: 1986

Country: Spain

Estimated turnover in 2023: €40-50m

Pescatrade is one of the few prominent importers in Spain without a cooking facility. The company offers a wide range of frozen fish and seafood products and supplies the wholesale and retail market.

France

France has a relatively large market for frozen shrimp compared to Spain; hence, many suppliers are active in the marketplace. At least 40 companies directly import frozen Penaeus shrimp from Africa, Asia, and Latin America. This brief overview lists the most prominent players not yet mentioned in French importers' chilled and cooked overview. This overview includes direct importers and one or two companies that process significant quantities and source (primarily) from importers. These players supply large-scale retail and food service companies but sell to wholesalers in the fragmented Horeca segment.

Picard

Founded: 1906

Country: France

Estimated turnover in 2023: €1.8b

Owned by: Invest Group Zouari

Picard is a specialized frozen food retailer. Its product range includes shrimp in raw, cooked, marinated, breaded, and ready-meal forms. All products are packed under its private label. The company operates more than 1,000 stores in France and, under the ownership of Zouari, is expected to expand internationally. Picard does not import directly but is supplied by other importers. Picard emphasizes sustainability; all its shrimp products are MSC, ASC, Label Rouge, or organic certified.

Escal

Founded: 2014

Country: France

Estimated turnover in 2023: €150-160m

Escal is a family-owned company that started selling French specialty products on the German market. Today, the company offers retailers a range of seafood, snails, and specialty products, mainly in Germany and France. The seafood business accounts for around 60% of the company’s total turnover, and shrimp is responsible for most of it. Escal is a strong brand that sells farmed and wild-caught shrimp, including some organic shrimp products. Its L. vannamei shrimp is mainly imported from Ecuador, India, and Vietnam. In 2020, Escal acquired shrimp cooker L’Assiette Bleue and entered the chilled and cooked shrimp market, focusing on non-treated products.

Gelazur

Founded: 1960

Country: France

Estimated turnover in 2023: €80-100m

Gelazur is a French importer specializing in frozen shrimp (primarily ASC, MSC, and organic certified products) and other seafood products. The company imports around 10,000 MT yearly and sells mainly to large-scale food service, wholesale, and retail segments in France, Italy, and Spain. It sources farmed and wild-caught shrimp from Ecuador, India, and other countries worldwide.

Eurotrade Fish

Founded: 1978

Country: France

Estimated turnover in 2023: Unknown

Eurotrade Fish claims to handle more than 1,000 containers annually. This represents around 20,000 MT of product, of which a significant part is L. vannamei shrimp, but the company also trades Argentinian red shrimp, hake, and other seafood products. Regarding shrimp, the company has representation agreements with companies such as Arengus in Argentina and Omarsa and Edpacif in Ecuador. Eurotrade works with cookeries and other processors to supply shrimp to retailers and wholesalers in France and other countries in the South of the EU.

SN Trading

Founded: 2014

Country: France

Estimated turnover in 2023: €40-50m

SN Trading is a significant importer of frozen shrimp and supplies cookeries and wholesalers in France and Spain with bulk products. It is a specialized shrimp trader from Latin America with highly standardized products. The company claims on its website that it sources shrimp primarily from (in order of significance) Venezuela, Ecuador, Peru, and Colombia and sells around 12,000 MT yearly. The company’s sales volume tripled between 2014 and 2023.

Gelpeche

Founded: 1984

Country: France

Estimated turnover in 2023: €40-50m.

Owned by: Groupe JMI

Relevant group companies: Crusta C (France), Nov’East Seafood (Romania), Refripeche (Madagascar)

Gelpeche is the leading frozen seafood importer and distributor within the JMI group. It sells wild-caught and farmed shrimp to the retail and food service segments. The shrimp is sourced from its group companies and trading partners in Madagascar, Ecuador, and France. Gelpeche also imports farmed L. vannamei and P. monodon and wild-caught shrimp from Asia, especially India.

Si2A

Founded: 1991

Country: France

Estimated turnover in 2023: €30-40m

Si2A is a medium-sized frozen shrimp importer and trader that imports around 5,000-6,000 MT yearly, primarily from Latin America. On a smaller scale, the company also trades squid and cuttlefish. It mainly supplies the food service and wholesale segments.

Italy

Like France, Italy has a relatively large wholesale market for frozen shrimp. However, it’s fragmented, and many local and regional players supply the market. The companies listed here are the biggest importers nationwide and a few of the most prominent regional players, representing at least 2,500-5,000 MT each. Do you need more detailed information on other Italian shrimp importers? Let us know!

Marr

Founded: 1972

Country: Italy

Estimated turnover in 2023: €2b

Marr is Italy's largest frozen food wholesaler, with a 17% market share in a highly fragmented wholesale and food service market. The three companies that follow combined only have a 12% market share. According to the group, 25% of 213,000 foodservice operators in Italy are its clients. The company was established in 1972 and stocklisted in 2005. Its company records show that after a substantial drop during Covid, in 2023, it reached a €2b turnover. The company's financial records also show that 70% of its revenues come from ‘street sales,’ 10% from wholesale, 10% from canteens, and 10% from ‘chains and groups.’ The company has more than 40 distribution centers throughout the country, of which several are cash and carries. Seafood represents 30% of its revenues, and the group has several wild-caught and farmed shrimp items in its portfolio. The company imports directly from Ecuador, India, and possibly other South American and Asia countries.

Comavicola Commerciale Avicola

Founded: 1956

Country: Italy

Estimated turnover in 2023: €125-150m

While established back in 1956, the company started in seafood only in 1989. Today, Comavicola is one of Italy’s largest specialized frozen seafood importers, processors, and distributors. Initially, the company focussed on wholesale and food service, but in 2018, it opened a processing facility dedicated to retail packaging. Since 2023, the company also operates its cash and carry centers. It owns several famous brands that are well-known in their respective market segments. It sells shrimp from Ecuador under the ‘Re Mare (King Sea)’ and ‘Santa Maria’ brands, primarily sold wholesale and distributed to HORECA. Comavicola also imports small volumes from India, most likely wild-caught shrimp, for its ready-eat meal selection.

Panapesca

Founded: 1972

Country: Italy

Estimated turnover in 2023: €150-175m

Owned by: Xenon Private Equity

Relevant group companies: Thai Spring Fish

Panapesca claims to be Italy’s largest private label supplier to retail and wholesale chains. It operates a nationwide network of depots to cater to its customers and has its seafood shop named Bottega Marinara. The group owns a processing plant in Thailand (Thai Spring Fish) that packs Argentine red shrimp, L. vannamei shrimp, and other seafood products.

It offers a range of fresh and frozen products, including ready meals, several of which include shrimp. The company primarily supplies wild-caught Argentine red shrimp but has several items, including farmed L. vannamei shrimp products. It’s not one of Italy's most prominent players in farmed shrimp, but it is significant as an all-around seafood supplier to wholesalers and retail chains.

Skalo SPA

Founded: 1978

Country: Italy

Estimated turnover in 2023: €40-50m

Skalo was founded in 1978 and, according to the company, was the first company in Italy to import farmed L. vannamei from Ecuador in 1985. In the 1990s, the company also started importing cephalopods from India and a range of European seafood products. With the second generation of the family that owns it having taken over, the company has diversified into fresh fish. It has developed a substantial processing and distribution operation to supply the large and fragmented wholesale market. It is one of Italy’s top five importers of Ecuadorean shrimp.

Axel Food SRL

Founded: 2014

Country: Italy

Estimated turnover in 2023: €40-50m

Axel Food is a relatively new regional wholesaler based out of Milan. It offers a wide range of seafood products and has several Argentinian red and vannamei shrimp items in its portfolio. Within a few years, the company has become one of the leading importers of Ecuadorean shrimp on the Italian market. It also imports value-added items from Asia. Its Ecuadorean shrimp is sold under the Santa Maria and Luna brands. Axel Food is closely linked to Comavicola, working together on sourcing and logistics. The two companies sometimes also co-exhibit.

Portugal

As we have seen in the statistics session, Portugal is a small importer of Penaeus shrimp, around 25,000 MT in 2023. Add another 8,000 MT of other species to that, bringing the total to 33,000 MT. Spain is the largest supplier (50%). Direct imports come primarily from Ecuador (25% of total direct imports) and India (25% of total direct imports). Brasmar is the largest importer, representing around 20% of direct imports. All other importers, a group of 20-30 companies, represent less than 1,000 MT each. Nueva Pescanova and Grupo Profand are believed to be significant suppliers from their facilities in Spain.

Brasmar

Founded: 2003

Country: Portugal

Estimated turnover in 2023: $250-350m

Owned by: Vigent Group and MCH Private Equity

Brasmar Group is an importer of shrimp and a large producer of a wide range of seafood products, which it sells in the Portuguese and other European markets. It has processing plants in Portugal, Spain, and Norway and a sales network throughout Europe, Brazil, and the US. Its most important products are cod and octopus. As part of its portfolio, it offers a range of frozen shrimp products.

Greece

As we have seen in the statistics section, Greece only imports around 7,500 MT of Penaeus shrimp (primarily of Ecuador origin) and an almost equal amount of wild-caught shrimp (primarily of Indian origin). A variety of wild-caught shrimp (mainly Asian pink and Argentinian red) is offered in supermarkets. The biggest shrimp importer in Greece is Pescanova Hellas, believed to represent around one-third of total Greek Penaeus imports. At least 10 to 15 other companies also import frozen Penaeus shrimp in relatively small amounts. The two most prominent shrimp importers besides Pescanova Hellas are thought to be Ch J. Pantazis and Vasilou Trofinko, both present in the retail and wholesale segments.