On 18 August 2021, I will present at the virtual TARS Aquaculture Conference, the leading shrimp industry venue, where mainly Asian industry stakeholders meet to discuss the current status and outlook of the Asian shrimp industry. This year the meeting will take place digitally from 18 to 20 August. To attend, register here. My presentation will briefly review the impact of COVID-19 on EU shrimp imports and provide an outlook of the EU shrimp market up to 2022. However, more importantly, I will look back a little further and show how Asian shrimp exporters are losing their market share in the EU and reflect on whether Asian shrimp has a future in the EU. In this blog, I will provide you with a preview of what I will present on 18 August.

This blog is sponsored by Grobest, Skretting, Inve Aquaculture, DSM, American Penaeid Inc., Zeigler Nutrition, and Aqua Pharma Group.

2020 Was Not a Bad Year for Total EU Raw and Blanched Penaeus Imports, which Grew from 255,000 MT to 269,000 MT

COVID-19 was bad for the EU food service industry and good for the EU retail industry. But it was not as bad for the food service industry as people thought it would be. During the summer of 2020, when the first wave of COVID-19 came to an end, people went out dining quite a lot. Restaurants’ suppliers could sell their stocks. While delayed containers started to arrive in July and August, they were not sufficient to meet demand, and new orders were placed from July onwards. The second wave of COVID-19 caused new lockdowns to be reinstated during winter. Then, in the spring of 2021, the situation became more under control, and, gradually, society started reopening. Now, during summer, EU consumers are ready to enjoy life, and, among other things, shrimp, again.

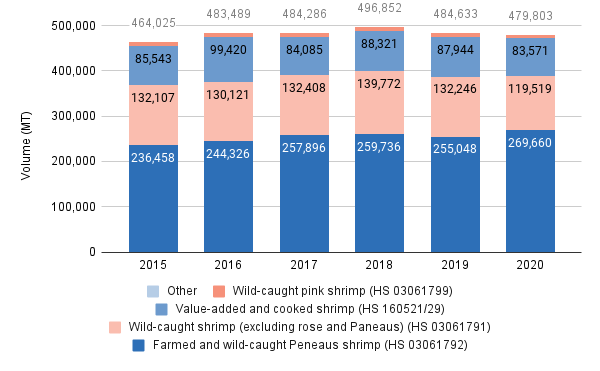

Figure 1: EU shrimp imports from 2015 to 2020

Source: EUROSTAT

Note: In this blog the EU refers to the EU 27 and excludes the UK

Looking at how this translates into statistics, imports of raw and blanched Penaeus shrimp (HS 03061792) – mainly L. vannamei and partly P. monodon – increased from 255,000 MT in 2019 to 269,000 MT in 2020 (see Figure 1). This is interesting because the EU’s total shrimp imports slightly contracted from 484,000 MT in 2019 to 479,000 MT in 2020. It was mainly the import of Argentinian wild-caught shrimp (HS 03061791) that declined. The increase in imports of Penaeus shrimp and the decrease of imports of other species confirms that L. vannamei is mainly a retail product, as opposed to the other species that are primarily food service products for out-of-home consumption. Value-added and cooked shrimp imports from Asia and South America slightly contracted from 32,000 MT to 31,000 MT.

Due to logistical challenges and disappointing harvests this year, importers currently have trouble sourcing sufficient products. Although demand is there, especially now that most lockdowns are coming to an end, most importers only seem to be able to meet immediate demand but are unable to build new inventories. This is good news for suppliers! It means that, most likely, demand will continue to be strong after this summer and maybe even until next year’s first crop in March or April. Farmgate prices may therefore remain favorable, unless farmers decide to produce a monster crop that the market cannot absorb.

Although 2020 Was Not a Bad Year for Penaeus Shrimp’s Volume in the EU, It Was a Lousy Year for Asian Suppliers

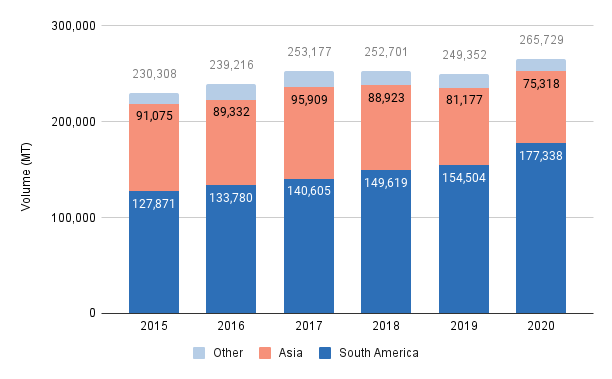

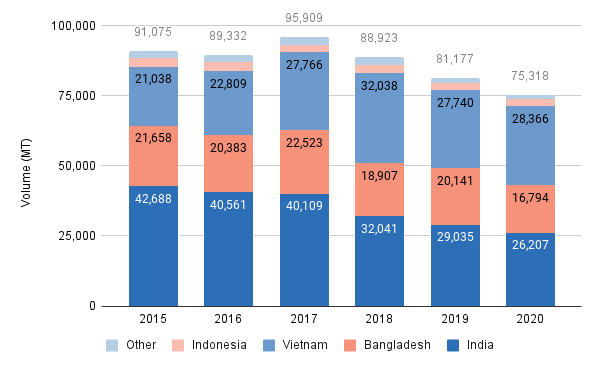

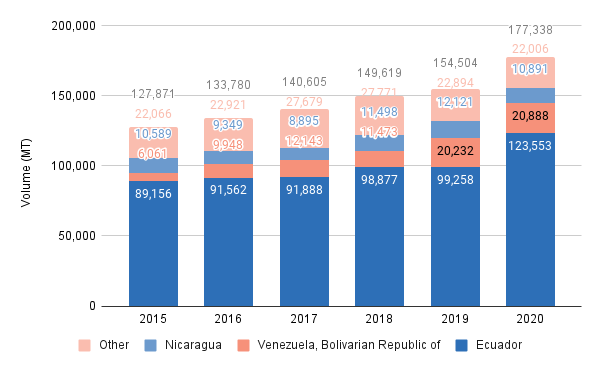

Interestingly, it was not Asia that grew its Penaeus exports (HS03061792) to the EU. On the contrary, EU imports of Penaeus shrimp from Asia contracted by 6,000 MT, while imports from South America grew by almost 23,000 MT (Figure 2). Within Asia, it was mainly India and Bangladesh that saw their exports drop; India from 29,000 MT to 26,000 MT and Bangladesh from 20,000 MT to 17,000 MT. Vietnam managed to increase its exports slightly but possibly not as much as might have been expected with the Free Trade Agreement (FTA) with the EU in place. Its exports to the EU increased from 27,700 MT to 28,400 MT. Jointly, India, Bangladesh, and Vietnam account for 95% of total Penaeus imports from Asia. In South America, it was mainly Ecuador that increased its exports; from 99,000 MT in 2019 to 124,000 MT in 2020.

Looking at the Long-Term Trend, the Situation Is Even Worse, and Market Share of Asian Suppliers Is Down to 28%

If we only look at 2019 and 2020, we might attribute Asia’s contraction to all the challenges that producers were confronted with due to COVID-19: lockdowns, disruptions of processing operations, and shortage of containers for transport. At the same time, the surge in South American products might be attributed to the fact that Ecuador had a lot of trouble shipping its products to China and therefore had to sell them into the EU and US markets at rock-bottom prices. Although these reasons may have played a role in last year’s trade flows, attributing all of the decline to COVID-19 distracts from the fact that trade data reveals a longer term trend as well (see Figure 2).

Figure 2: EU imports of Penaeus shrimp (HS03061792) between 2015 and 2020

Source: EUROSTAT

Especially India’s Exports to the EU dropped, and Vietnam has Become the Largest Exporter to the EU

The share of Asian shrimp on the EU market has been declining for some time now; between 2015 and 2020, supply fell from 91,000 MT to only 75,000 MT. India’s exports dropped from 43,000 MT in 2015 to only 26,000 MT in 2020, which is mainly the result of the ongoing pressure of the EU on India to resolve issues related to use of antibiotics in its shrimp industry. Whether they are justified or not, measures such as additional container checks and the threat of being removed from the EU-approved exporter list caused many Indian exporters and EU buyers to look for partners elsewhere. There is no sign that the Indian and EU authorities will resolve their dispute soon.

Figure 3: Asia’s exports of Penaeus shrimp to the EU between 2015 and 2020

Source: EUROSTAT

With 28,000 MT of Penaeus shrimp under the HS 03061792 code and an additional 20,000 MT under the HS 160521/29 code (which accounts for 70% of the EU’s total imports under this code), Vietnam has overtaken India as the EU’s largest supplier of Penaeus shrimp. While Vietnam’s exports increased between 2015 and 2018, they have dropped a bit since then. This is surprising as the EU-Vietnam FTA gives the country a competitive edge over most other Asian suppliers.

Surge in South America’s Exports to the EU Thanks to Ecuador and Venezuela

Between 2015 and 2020, South American shrimp supplies increased from 127,000 MT to 177,000 MT and now have a 67% market share in the EU. Ecuador and Venezuela account for the most significant part of this surge; while Venezuela was responsible for the largest increase between 2015 and 2019, Ecuador accounted for the entire surge between 2019 and 2020 (see Figure 4).

Figure 4: South America’s exports of Penaeus shrimp to the EU between 2015 and 2020

Source: EUROSTAT

Of course, last year’s increase was partly due to Ecuador’s problems in China and its need to divert to other markets. Ecuador’s key market in the EU is still southern Europe, and Spain absorbed most of Ecuador’s surge in exports. However, the market in northern Europe is also growing; from 5,000 MT to 6,000 MT between 2015 and 2019, only to double to 12,000 MT in 2020. Although still a small market, the increase in exports to northern Europe is of utmost importance for Asian suppliers to look into.

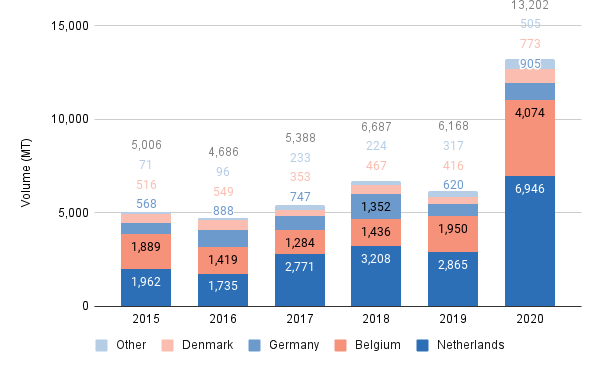

The Netherlands and Belgium Account for Almost All Imports of Ecuador’s Shrimp into North-Western Europe, Which Ends Up Mainly in the Refreshed Supermarket Segment

The Netherlands and Belgium are responsible for almost the entire surge in northern Europe’s imports from Ecuador (see Figure 5). Companies like Heiploeg, Klaas Puul, Seafood Parlevliet, and Shore import Ecuadorian shrimp, reprocess it and then export it to supermarkets across the EU.

Figure 5: Ecuador’s exports to north-western Europe

Source: EUROSTAT

In The Netherlands, South American Shrimp Ends Up Mainly in Supermarkets’ Refreshed Segments

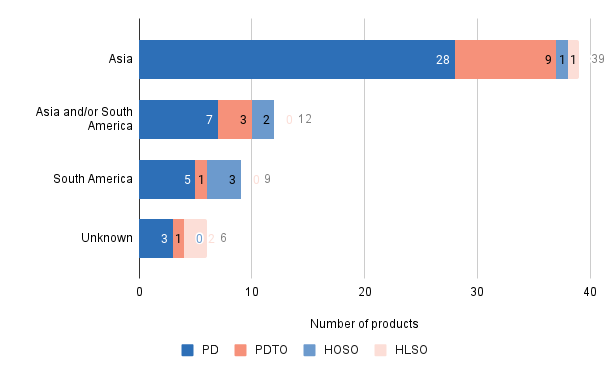

Taking a look at the web shops of some of the leading supermarkets in north-western Europe shows that shrimp from Ecuador and other South American suppliers is no longer only sold as an organic or conventional head-on shell-on (HOSO) product. Although these supermarkets are still dominated by Asian products, peeled products increasingly originate from Ecuador and other South American countries (see Figure 6).

Figure 6: Origins of L. vannamei products in Albert Heijn, Jumbo, and Plus supermarkets in the Netherlands in 2021

Source: web shops of Albert Heijn, Jumbo, and Plus supermarkets in the Netherlands

In May and June 2021, in the three largest supermarkets in the Netherlands, 21 out of 66 farmed L. vannamei shrimp products were sourced from South American countries. 12 of these products were peeled and deveined (PD), 4 peeled and deveined tail-on (PDTO), and 5 were head-on shell-on (HOSO). 18 of the products were sold as a refreshed products. 2 of the 3 frozen products from South America were HOSO, and 1 of them was PD and organic certified.

The fact that peeled South American shrimp is mainly found in the refreshed segment indicates that South American suppliers are not yet competitive with frozen products packed at origin: Asian suppliers still dominate this segment. However, reprocessors in the Netherlands and Belgium – such as Heiploeg, Klaas Puul, Seafood Parlevliet, and Shore – play a crucial role in introducing South American products into the refreshed segment and importing them in bulk.

Ecuador Entering the Mainstream EU Retail Market Is a Direct Threat to the Position of Asian Competitors

Of course, one reason why Ecuador and Venezuela experienced increased sales to the EU is that their prices have been very competitive. Their relatively extensive farming systems lead to lower feed conversion ratios and result in lower production costs. Moreover, these countries are not confronted with a lot of regulatory control and added costs for shipping to the EU in the same way that India is. Even though labor is more expensive, production costs in Ecuador have been so competitive that the country has started to compete with Asian prices for peeled shrimp. However, under the surface, there’s a lot more to it than just prices.

Driven by a need to diversify its markets and a desire to sell at higher prices than its competitors, Ecuador’s shrimp industry has heavily invested in building a brand that positions Ecuador’s shrimp as the best shrimp in the world. And whether you like it or not, it works. Collective marketing by the Chamber of Aquaculture (CnA) and the recently established Sustainable Shrimp Partnership, combined with individual marketing efforts of leading producers such as Omarsa and Songa, contribute to Ecuador’s shrimp being perceived as a premium product. Indirectly, most other South and Central American suppliers benefit from Ecuador’s marketing efforts; buyers often compare South American shrimp to Asian shrimp without differentiating between countries within the two continents.

Although already having an established market in southern Europe, almost every supermarket purchase manager I talked to in north-western Europe wants to add Ecuadorian products to their portfolio. Facilitated by EU importers and processors such as Heiploeg, Klaas Puul, Seafood Parlevliet, and Shore, they have started doing just that.

Asian Shrimp Producers Need to Reflect on Their Strategy and Start Thinking about Collective Action to Safeguard Their Market in the EU

So is there a future for Asian shrimp in the EU? Definitely! But it’s time for Asian producers to start working together, to look into the mirror, and to make some changes in how things are done. Production decisions should not only be made from a production perspective. Producers need to look at the market, analyze it, and see how their capabilities and products could fit in. To counter the surge of Ecuadorian and other South American producers in northern Europe’s market for peeled shrimp, Asia’s suppliers need to start competing not only on the price, but also on the quality, sustainability, and perception of their products. And this is what I will elaborate on during the first day of the virtual TARS Aquaculture Conference on Monday 18 August.