Attracting finance and investment has always been a major bottleneck for the tropical aquaculture industry. For international commercial banks and development finance institutions (DFIs), investing in companies that are involved in the production of live animals is often regarded as being too risky. This is even more the case for aquaculture, which also still faces many of the challenges of a nascent industry. International commercial banks and DFIs are willing to invest in feed companies, and are increasingly ready to finance and invest in vertically integrated producers. But they are often not yet at the point of wanting to directly invest in or finance farming operations. Besides the level of risk and the ability of companies to offer collateral, this is also often related to the size of operations: the ticket sizes required by international commercial banks and DFIs are often so large that only a few tropical aquaculture companies fit the profiles they’re looking for. However, now the tropical aquaculture industry is coming to maturity, this scenario may slowly be changing. In this blog, I want to take a brief look at aquaculture in Vietnam and see whether opportunities for finance and investment exist.

This blog is drawn from an analysis that I conducted in partnership with Anton Immink of Think Aqua and the Shrimp Blog is sponsored by Grobest, Skretting, Inve Aquaculture, DSM, American Penaeid Inc., Zeigler Nutrition, Aqua Pharma Group and VASEP..

VIETNAM IS ASIA’S FOURTH-LARGEST AQUACULTURE PRODUCER AND SECOND-LARGEST SEAFOOD EXPORTER

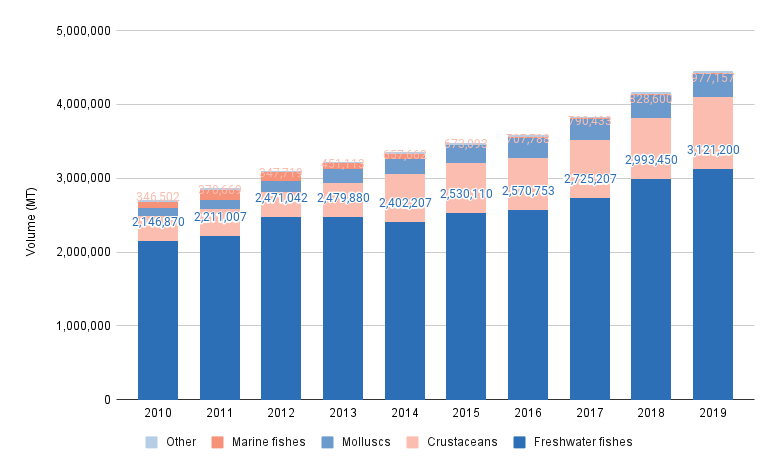

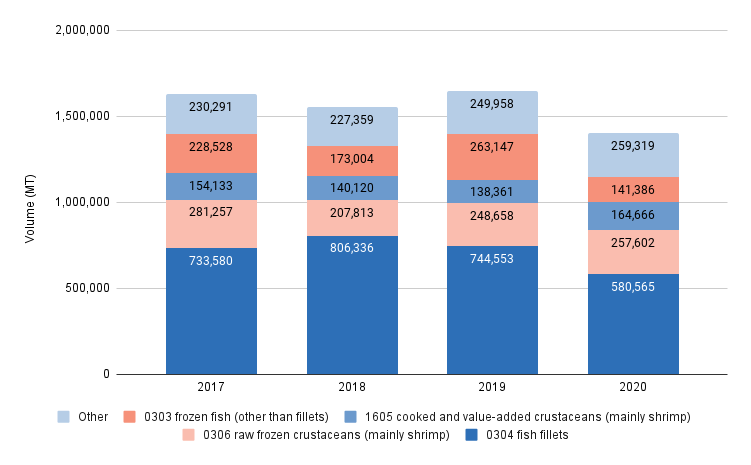

According to the Food and Agriculture Organization of the United Nations (FAO), with 4.5 million MT per year worth $12bn, Vietnam is the fourth-largest producer of farmed fish and seafood in Asia. In terms of exports, it’s Asia’s second-biggest seafood exporter after China exporting 1.5 million MT per year at a value of almost $8bn. Vietnam’s aquaculture industry is dominated by the production of finfish (pangasius, carp, and tilapia) in freshwater and shrimp (Pacific white and black tiger) in brackish water. Production has been increasing, but pangasius and shrimp have been the most important drivers of growth. Shrimp and fish fillets (pangasius is mainly exported as fillets) represent 45% and 32% of total exports respectively. Producing just over 330,000 MT worth $3.3bn, Vietnam is Asia’s second-largest shrimp exporter (after India). It’s also Asia’s second-largest fish fillet exporter (after China) at 800,000 MT per year worth $2.5bn.

Figure 1: Vietnam's aquaculture production

Source: FAO

Figure 2: Vietnam's seafood exports

Source: UN Comtrade

PANGASIUS AND SHRIMP ARE THE MOST INTEGRATED AND CONSOLIDATED AQUACULTURE SECTORS IN VIETNAM

Although to different degrees, both the pangasius and the shrimp supply chains in Vietnam are becoming increasingly vertically integrated and consolidated as companies at various levels of them tend to include more than one activity in their operations and have scaled significantly. While some of the vertically integrated companies as well as some feed companies are active in both pangasius and shrimp, the two supply chains operate relatively independently from each other. This might be due to the opposite commercial nature of the two species: pangasius is a low-value high-volume product while shrimp is a high-value low-volume product.

While most of the feed companies don’t publicly disclose their revenues, some of the vertically integrated producers are listed and their numbers are public. In 2020, the largest shrimp producer, Minh Phu, had a revenue of over $623m. At quite some distance behind it is PAN Group’s FIMEX—the second-largest publicly listed vertically integrated shrimp producer—with revenues of $192m, and other not publicly listed companies like Stapimex come close behind. In 2020, Vinh Hoan, IDI Corporation, and Navico, the three largest publicly listed pangasius producers, had a revenue of $306m, $276m, and $150m respectively. Just like most of the feed companies that normally operate at a larger scale, these vertical integrators and feed companies are of a size that fits the ticket size requirements of most international commercial banks and DFIs.

THE TOP FIVE PANGASIUS COMPANIES ARE LIKELY TO FURTHER EXPAND THEIR MARKET SHARE OVER THE NEXT COUPLE OF YEARS

Even though production in other countries, like in Bangladesh and Indonesia, is on the rise, today the producers in these countries are not competitive on quality and price with Vietnamese producers. While earlier it consisted of many small-scale farmers, today the pangasius supply chain is the most consolidated and vertically integrated of Vietnam’s aquaculture industry, and it’s largely export-oriented. The sector is dominated by large-scale operators that have vertically integrated breeding, farming, processing, and sometimes also feed operations. Some of the largest integrators are Vinh Hoan, IDI Corporation, Navico, Hung Vuong, GODACO, and Biendong.

A price crash in the second half of 2019, which occurred after a rise in production in 2018 and the first half of 2019, shows that the international market is not ready to absorb large volumes of pangasius without having prices drop. As a result, further consolidation is likely to happen, and I expect that larger vertically integrated producers will increase their share of production over the next couple of years. There are between 5 and 10 producers that are likely to dominate the market and some of them have massive farm expansion projects in the pipeline. The most impressive project is perhaps that of Navico, which has recently invested in a new project called “Nam Viet Binh Phu.” Once at full capacity, this will be the biggest pangasius farming and breeding project with an investment of $170m and more than 600 ha. The company could reach a 15-20% market share, and its total export value could grow to $300m.

Video 1: Navico's 600 ha Binh Phu pangasius farming project

Some of the larger producers have invested in integrating feed production into their supply chains, but it’s doubtful whether this trend will continue. The recent sale of the feed activities of two major vertical integrators, Huong Vuong and Vinh Hoan, might be an indicator that vertically integrated pangasius feed production can’t compete with larger broadline animal feed producers, and that, while previously it was necessary for integration in order to grow, the industry is now reaching a level of maturity that means even higher levels of scale are needed to remain competitive.

In general, looking at the size of Vietnam’s integrated pangasius producers, the top five producers may now have reached levels of scale that make them candidates for investment from international commercial banks or DFIs. However, the fact that the growth of the pangasius sector may have plateaued could mean that banks and DFIs become more cautious about investing in large companies that do not stay at the forefront of developments and choose to back only those large producers that are making the right investments in innovation to access more of the benefits of scale and higher levels of efficiency.

THE SHRIMP SECTOR IS POISED FOR GROWTH BUT IT REMAINS FRAGMENTED

Video 2: Vina Cleanfood's 150 ha super-intensive shrimp farm

The shrimp industry is less consolidated and integrated than the pangasius industry. This is especially the case for the farming segment. The largest part of shrimp production in Vietnam is still done by small-scale farmers who buy inputs from dealers and sell their shrimp through middlemen. There are tens of thousands of small-scale farmers in the Mekong Delta. But there’s also a growing number of corporate farms, some of which take shrimp farming in Vietnam to the next level. In general, shrimp is perceived as an even more risky species than other fish and seafood. Among other things, this is due to the fragmentation of the shrimp supply chain, disease-related challenges, and the use of marine ingredients in shrimp feed.

Despite the associated risks, shrimp processors and exporters in Vietnam increasingly invest in farming. The main reason is to secure ASC and/or BAP-certified raw material for their retail program business, especially in the EU and US. These investments in farming can either be through direct ownership or through contract farming arrangements with individual farms or farmer cooperatives. Most current investment in farming takes the form of working capital for contract farming arrangements. But many exporters, such as Minh Phu, Fimex, BIM, and Vina Cleanfood, have invested in larger corporate farms as well. These farms must, in turn, guarantee the exporters a minimum volume of supply so that they can ensure supply for the contracts of their most important clients. Besides Minh Phu, some of these companies, such as Fimex, have reached such levels of scale and integration that they’ve become possible candidates for investment from larger banks and DFIs. To date, Minh Phu is one of the few companies that has attracted significant foreign investment; Japan-based conglomerate Mitsui has acquired a significant share of Minh Phu’s stocks and is acting as a strategic partner to further develop Minh Phu’s business, including further vertical integration of shrimp farming. Investments in these large, vertically integrated companies may also be used to provide them with more working capital to engage larger numbers of farms in contract farming arrangements where they get access to inputs at better terms.

The rise of super-intensive farming technology in Vietnam’s shrimp farming sector deserves some additional attention. Hatchery operators like Viet-Uc, Thong Thuan, and Duong Hung, and processors such as Minh Phu, CP Vietnam, and Vina Cleanfood have recently invested in super-intensive farming systems. These companies are in the process of setting up (semi-)indoor shrimp farms which produce at densities of anywhere between 200-500 pcs/m2, much higher than conventional farms in Vietnam which would stock somewhere between 100-200 pcs/m2. Although the potential of super-intensive farming in terms of more efficient use of land and water is large, the success rate of these systems must still be proven. The risk involved requires a different type of farmer who is able and willing to adopt technologies and acquire the skills required to manage these types of farms successfully. Investing in these companies might therefore be considered too risky, but ultimately these companies could come out on top in the future.

OPPORTUNITIES IN FEED

Foreign companies such as CPF (Thailand), Grobest (Taiwan), Uni-President (Korea), Shenglong (China), Tongwei (China), and Skretting (the Netherlands) dominate the shrimp feed market. Contrary to pangasius, in shrimp, except for Minh Phu, not many of the large vertically integrated shrimp producers have integrated feed into their supply chains. But the feed companies do play an important role in the supply chain: they run demonstration farms, provide technical support to farmers, and guide them towards more efficient—and often more intensive—production systems. They have, in some cases, also invested in hatcheries to provide farmers with high-quality PL in a package with their feed. Most of the shrimp feed producers also produce high-value marine fish feeds, which, just like shrimp feed, require more demanding formulations and sophisticated production facilities compared to freshwater fish and other animal feeds.

Contrary to shrimp feed, in pangasius feed, local producers (like Proconco (the largest producer), Co May Group, Hoang Long Group, and Vietnam Greenfeed) dominate the market. Most of these companies are broadline animal feed producers, and besides freshwater fish feed, they also produce poultry and pig feed. Only a few of the pangasius feed producers are dedicated aquafeed producers, and some of those that once were are now being acquired by other more diversified companies as they struggle to compete with larger animal feed producers. For example, Vinh Hoan (the number one pangasius feed producer) sold 85% of its feed subsidiary to Pilmico. Huong Vuong, previously also a major producer, leased out much of its capacity to Cargill.

In general, both the pangasius and shrimp feed sectors are currently operating at overcapacity. But while the shrimp industry is projected to grow significantly, the expansion of pangasius and other freshwater fish is not expected to be exponential. Therefore, investing in shrimp feed may well be a good opportunity, while investments in pangasius feed may be tricky business.

CONCLUSION

Although aquaculture in general—and shrimp in particular—may be viewed as a risky business, there are companies out there that are making the right steps to manage these risks and develop the aquaculture and shrimp industry in a sustainable and responsible manner. For these companies, access to finance and investment is often a crucial element to furthering business expansion, and this bottleneck often holds them back from reaching their potential. I hope that by shedding some light on the industry in Vietnam, banks and DFIs will be inspired to look at investment opportunities with some of the companies that are drivers of change in the industry.