In 2019, I published the Shrimp Insights Guide to the L. vannamei Broodstock Market. In 2022 and 2023, I provided you with an update, but I skipped 2024. So, it is time for the next update. It has been turbulent, with one of the major players filing for bankruptcy, three companies engaged in M&A, and a few others aggressively expanding their operations.

Disclaimer: These numbers have been self-reported by each company except Benchmark and Viet-Uc, for which I made a rough estimate.

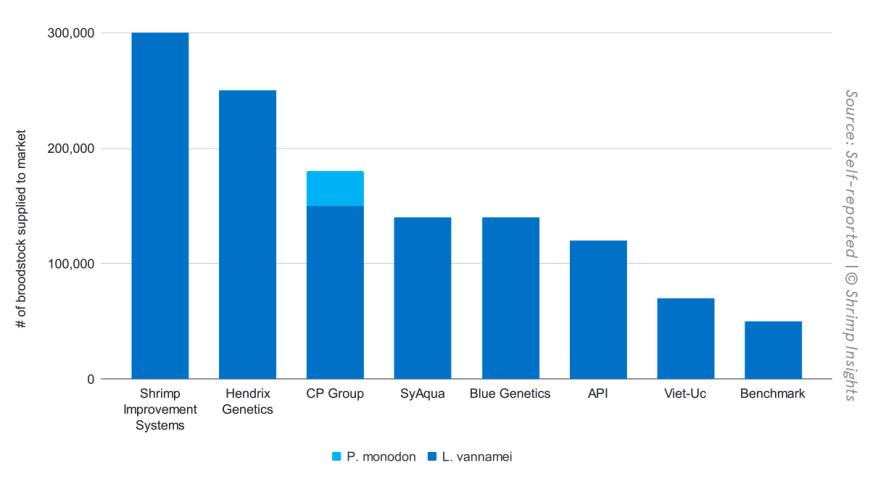

While the company names in the top five world broodstock suppliers remain the same, their order has changed, and the list of broodstock suppliers has shortened. The top five in 2024 was led by Shrimp Improvement Systems, followed by Hendrix Genetics, CP Group, SyAqua, and API. Blue Genetics from Mexico and the US, Benchmark Shrimp Genetics from Colombia and the US, and Top Aquaculture from Thailand complement these five companies. Local breeding companies such as Viet Uc in Vietnam, Prima Larvae in Indonesia, and Haid in China are some of the genetics suppliers in Asia.

In this blog, you will find an update on the broodstock market in the world’s most important markets and company updates from the world’s largest broodstock suppliers.

In 2025, the Shrimp Blog is supported by: Bioiberica, DSM-Firmenich, Fisherman's Choice, I&V-BIO, INVE Aquaculture, Megasupply, Omarsa, Shrimp Welfare Project, The Waterbase Limited, and Wanaka Seafood.

Key Company Observations

- Shrimp Improvement Systems is most likely the world’s largest broodstock supplier, selling around 300,000 in 2024. It is the largest supplier of broodstock to Vietnam and India and has a strong position in Indonesia and China.

- Hendrix Genetics’ BMCs in India, Indonesia, and Thailand are in full swing. As a result, its facility in Hawaii increasingly ships PPL instead of adult broodstock, whereas its facilities in Asia ship adult broodstock to their hatchery clients. Despite a substantial drop in sales to India, the company increased shipments to other countries. It claims to have sold around 250,000 SPF broodstock across the globe in 2024.

- CP Group continues to supply its subsidiaries and customers in South and Southeast Asia from its facilities in Thailand. To reach markets from which its Thai facilities are banned, it is expanding its HomeGrown Shrimp and CP Florida operations in Florida, USA. The company has shipped around 180,000 animals, of which 150,000 were L. vannamei and 30,000 P. monodon.

- SyAqua is the broodstock sector’s fastest-growing supplier, aiming to increase sales from 140,000 in 2024 to 200,000 broodstock in 2025. The company has optimized its operations in Florida and Thailand and acquired US-based Primo Broodstock to expand its capacity further. The company has aggressively gained market share in India and continues to grow its business in China, Indonesia, and other South and Southeast Asian markets.

- Groupe Grimaud, in 2023, after acquiring Sea Products Development and merging its operations with its shrimp genetics division Blue Genetics, has recently made public that it is looking to sell all its shrimp genetics activities. Grimaud aims to sell the company to a strategic investor who can take the company to the next phase of growth. The company claims that in 2024, it supplied 140,000 broodstock to the market, including sales through its BMCs in India and Thailand.

- American Penaeid Inc. went through turmoil due to the impact of two hurricanes on its facilities in 2024. The turmoil led to the short-term departure of its CEO, Robin Pearl, and to filing for bankruptcy. After Robin’s return, the company is motivated to regain market confidence and regrow its broodstock business over the next few years. Its sales in 2024 dropped to 120,000 pieces.

- Benchmark sold its genetics business to Starfish Bidco, a subsidiary of Norway-based Novo Holdings. It’s unclear what the impact of this sale will be on the shrimp genetics division. In late 2024, the company reported breakthrough results in genetic resistance to some significant shrimp diseases. Its sales are thought to be below 50,000 pieces in 2024.

Ecuador

Before we go to Asia, let’s briefly touch on Ecuador. Ecuador does not import SPF broodstock. Instead, several companies run their own breeding programs. In a recent study conducted by Shrimp Insights, we discovered that while eight companies have the capacity for nauplii production, Texcumar holds 50% of the market share. Biogemar (part of Grupo Almar) is the second largest producer of Nauplii, but unlike Texcumar, it does not sell to the open market. Other companies that have maturation capacity include Santa Priscila, Naturisa, Aquagen, Hendrix Genetics, and Maduracion Marcor.

All other hatchery groups buy their nauplii from these seven companies and only grow nauplii to PL. Texcumar is the second largest player in PL production and, in terms of capacity, has less than 10% market share. The biggest PL producer in terms of capacity is Santa Pricila. Grupo Almar, Genemar, and Omarsa complement the top five. Where there are less than 10 companies involved in maturation, there are around 100 companies engaged in PL production. Illustrating the fragmentation of this part of the value chain.

Shrimp Improvement Systems

Shrimp Improvement Systems operates a Nucleus and BMC in Hawaii and a nucleus and BMC in Florida. The two facilities function as backups for each other, and the company can strategically decide from which facility it will supply where. Usually, the BMC in Florida would primarily supply India (disease-tolerant lines), while the BMC in Hawaii would primarily supply Vietnam and China (fast growth lines).

In terms of market shares, the company continues to dominate broodstock markets in India (50% market share), Vietnam (40% market share), and, to a lesser extent, Indonesia (20% market share) and China (<5% market share). In 2024, across its operations, the company supplied around 300,000 broodstock to the market, around the same number as in 2019 when I published the broodstock report.

Regarding the future outlook, the company continuously assesses opportunities to improve distribution and logistics, including the potential development of in-country BMCs. The company is doubling down on consolidating its position in India and Vietnam.. With a new management team in China, the company feels confident that it can continue growing its sales despite regulatory uncertainty and severe disease challenges.

CP Group

CP Group in 2024 supplied around 180,000 SPF broodstock to the market, of which 150,000 were accounted for by L. vannamei and 30,000 by P. monodon. The company has significant market shares in Vietnam, China, Malaysia, and the Philippines and expansion plans for India and Indonesia.

In 2023, one of the most significant developments in CP’s genetics business was opening its “Home Grown Shrimp” facility in the US. This facility was set up as a hatchery and a farm, aiming to supply PL to farms in and outside the US and grow shrimp for the domestic market. While successful as a hatchery, due to low prices and high costs, the company failed in its ambition to penetrate the domestic market and, in early 2025, announced it would shut down its consumer sales.

As an alternative strategy, the company is now aiming to use its facility in Florida as a Broodstock Multiplication Center (BMC) with a 100,000 capacity of two breeds– its Turbo (fast-growing) and its Kong (white spot tolerant and robust) lines. The broodstock is sold by its new company, CP Florida. The group will also maintain its licensing agreement with American Penaeid Inc. (API). As such, from its facilities in the US, CP can access markets that prohibit broodstock imports from Thailand, such as Indonesia and India.

The group will now be well-positioned to supply almost every market worldwide. It aims to supply L. vannamei broodstock from the US to South and Central America, India, and Indonesia. It also supplies its Turbo line from the US to the EU, where it has a broodstock arrangement with the hatchery of Noray in Spain and sells PL to various farms across the region. L. vannamei and P. monodon broodstock from Thailand will continue to be supplied to other Asian markets, such as China, Vietnam, Malaysia, the Philippines, and Bangladesh.

Regarding the Chinese market, CP Group says its sales are growing fast. It has started sales to several new large Chinese customers. According to the group, its Turbo line is a favorite of the small raceway greenhouse farms, rapidly expanding in South and Central China. Its Kong line competes with robust genetic lines of other companies, such as SyAqua and Shrimp Improvement Systems, for use in open ponds.

The company also claims demand for its P. monodon broodstock is stronger than ever. Sales are growing not only in China but also in Malaysia, Bangladesh, and Vietnam. The only limitation of its P. monodon sales is that it still does not have access to India and Indonesia. The company would have to start growing its P. monodon line in the US to access those markets.

India

India closed 2024 with overseas suppliers, and domestic BMCs supplied 193,379 broodstock to local hatcheries. This is down by 12% compared to 2023 and down by 30% compared to the peak in 2021. At an average value of around $85 per piece, the Indian broodstock market in 2024 accounted for around $16 million in sales. In this byte, I share the most important observations:

Overall:

- The downward trend of broodstock supplies is in line with the perception of Indian stakeholders that production in recent years has contracted, but not with the relatively stable exports of Indian shrimp. There seems to be a lack of clarity among Indian stakeholders about how to explain this. Some point toward the high-level inventories that Indian exporters had and may be sold and shipped to compensate for a drop in actual shrimp production. Others point toward the possibility that amidst the crisis that the industry was experiencing, hatcheries may have used first-generation broodstock for extended periods or produced second-generation broodstock domestically.

- Regarding the main hatchery groups, the L. vannamei PL market remains dominated by Vaisakhi Biomarine, Sapthagiri Group, BMR Industries, and Golden Marine Harvest. None of these represents more than 10% of broodstock supplies. The top four have a combined share of 28% of broodstock supplies. Previously, one of the most prominent players, CP Group, dropped out of the top four. In total, 87 groups were supplied with broodstock.

- While Shrimp Improvement Systems (SIS), with 50%, remains the market leader, SyAqua has grown its market share to 33% and has solidified its position in the Indian shrimp industry. Reportedly, SyAqua’s broodstock produces resilient PL in harsh environments and performs well while exposed to diseases common in Indian aquaculture. Hendrix Genetics-Kona Bay’s market share has dropped to 6%. The company has almost entirely halted its supplies of adult broodstock but instead has focussed on supplying its JV BMC with Sapthagiri Group with PPL. The BMC should start supplying adult broodstock to Sapthagiri’s and third-party hatcheries this season.

BMCs:

- In 2024, local BMCs in India received 530,823 PPL from overseas and domestic NBCs. This is triple the amount of 2023.

- The main driver of this growth is Hendrix Genetics and Sapthagiri’s BMC, which imported PPL almost every month and reached 357,663. Despite the BMC, Sapthagiri still imported 16,138 broodstock, primarily from SIS. In 2025, we should see this number drop and see supplies by the BMC increase.

- BMR Blue Genetics imported 85,378 PPL. Total imports by the BMC increased 15% year over year. BMR’s hatcheries only rely on 30% of its own BMC (L. vannamei), and the majority of broodstock in 2024 (44%) was sourced from SyAqua (L. vannamei). The remainder was sourced from SIS (L. vannamei) and Unima (P. monodon).

- Vaishnavi imported P. monodon PPL in December 2023, July 2024, and again in December 2024. The total in 2024 was 63,868, 18% down from 2023. As it takes six to eight months for PPL to grow into the size required to be transferred to the hatchery, July imports will be supplied to its hatcheries by January/February of the next year, and December imports will be supplied to its hatcheries mid next year.

- The RGCA BMC in Andhra Pradesh received 23,914 PPL from the RGCA NBC in the Andaman Islands. These supplies happened in early and mid-2024. The batch supplied in mid-2024 will be provided as broodstock to hatcheries in early 2025 and cater to this year's first crop.

P. monodon:

- In 2024, according to the CAA files, 13,222 P. monodon broodstock were supplied to hatcheries in India. This is a drastic 38% drop compared to 2024. However, this drop can be at least partly attributed to the fact that part of this year's shipments for the first season happened only in January 2025.

- Vaishnavi Aquatech is responsible for most of the drop. The company supplied 8,380 broodstock from its BMC to its hatcheries in November and December 2023, which were used for the first crop of 2024. Then, it supplied 2,800 broodstock from its BMC to its hatcheries in June 2024 and imported 858 adult broodstock from Moana in Hawaii. The company imported PPL from Hawaii in July and December 2024. These will be supplied to its hatcheries in Q1 and Q2 of 2025.

- Unima (Aquaculture de Mahajambal) supplied five hatcheries in 2024. Besides its JV in India (Unibio), the other hatcheries are BMR, Golden Marine, MAS Aqua Techniks, and Vaisakhi Biomarine. Its total supplies reached 6,939 broodstock. Besides supplying adult broodstock, Unibio will also provide Naiplii to the Sapthagiri group, which will not do maturation but use one of its hatcheries to grow Nauplii to PPL. Having a relationship with several of India’s major hatchery players makes Unima a crucial player in improving the availability of affordable P. monodon PL to Indian farmers.

- The RGCA BMC supplied early in 2024 broodstock to Tandels hatchery and Vaisakhi. However, it did not provide any broodstock in Q4 2024, so it seems it is not supplying broodstock for 2025’s crop unless these were shipped in January 2025.

- Having secured broodstock in Q4 2024, all top four hatchery groups can supply P. monodon PL to their clients for the crop of 2025.

Hendrix Genetics

Hendrix Genetics operates its NBC in Hawaii, selling adult broodstock to hatcheries worldwide and PPL to its BMCs in Indonesia, India, and Thailand. Besides that, it runs a breeding operation in Ecuador. In 2024, across all its operations, the company supplied around 250,000 broodstock to the market, up by around 50,000 compared to 2019, when I published my initial broodstock report.

In 2022, Hendrix Genetics entered a JV with Japfa to establish a BMC in Indonesia. Today, that facility is up and running and can produce around 80,000 broodstock yearly, with the option to expand quickly if needed. According to the company, the demand for broodstock in Indonesia declined by almost 20,000 pieces in 2024. Hendrix Genetics supplied around 70,000 broodstock, which equates to around a 70% share of the total market of 100,000 broodstock. According to the group, while having a JV with Japfa, most of its broodstock clients consist of other hatcheries.

In India, Hendrix Genetics opened its BMC in early 2024. This facility is a JV with Sapthagiri Hatcheries and can produce 160,000 broodstock. The company has been rebuilding market share after, in 2023, it was temporarily banned from the Indian market due to suspicion of the prevalence of pathogens in some of its broodstock. The company states the facility has run exceptionally well since commissioning and initial stocking. First sales commenced in July 2024, and the company’s clients reported excellent performance in the hatchery (which has always been a strong point). Farm performance is mixed. Extremely good in farms with high biosecurity and management practices. Mixed in more challenging farming environments.

As announced in the previous broodstock market update, Hendrix Genetics continues to expand its network of BMCs. The group has set up a BMC in Thailand. This facility was primarily built to expand its capacity to supply China. China remains one of the company’s most important markets, and its shipments to the country continue to grow. Its facility in Malaysia continues to provide the domestic Malay market. Vietnam is the only market in which the company has not significantly grown its business. The company explains that it has been working with selected partners to develop new lines that serve the needs of the Vietnamese market and hopes to grow its market share steadily.

Hendrix Genetics cannot provide further comments on what else is happening. It states that it's working through some opportunities and has exciting, significant news in the pipeline for 2025, which it can share in the coming months.

China

In 2022, I estimated that China used around 1.6 million broodstock annually, of which around half would be imported and half domestically produced. With these animals, China would create around 300 billion PL annually. The top 30 hatchery groups (according to “Southern Rural News, Agricultural Finance Book, and Great Fisheries”) are believed to produce around 250 billion PL annually and have an 80% market share. The top four on the list are Haid (58 billion PL), Tongwei (35 billion PL), Bohai Aquatic Products (30 billion PL), and Evergreen (13 billion PL). These are China’s largest shrimp conglomerates integrated into shrimp breeding. Some of these companies, like Haid and Evergreen, are known to have their integrated genetics programs.

It’s essential to break down the market into segments to understand the Chinese broodstock market. One part of the market has a strong demand for disease-tolerant and balanced lines, which have reasonable survival and growth rates in challenging environments. This market consists primarily of traditional shrimp farms, which grow shrimp in conventional earthen ponds. The other segment, the small greenhouses, and the indoor RAS farms, strongly demand fast growth lines. Most farmers using these systems take the risk of having more rapid growth to enable multiple crops per year. While production in the first segment is stagnant, output in the second segment grows fast, meaning that demand for fast-growth lines is currently the strongest.

Although official numbers are not available, it is clear that the market shares of broodstock suppliers have changed significantly. A few years back, API dominated supplies to the first segment, but today, it has lost most of its market share. Blue Genetics and SyAqua currently dominate supplies of disease-tolerant and robust lines. CP, Shrimp Improvement Systems, and Hendrix Genetics mainly service the second segment. Domestic broodstock producers gain market share in each segment at the cost of imported broodstock. P. monodon hatcheries are primarily supplied by CP Group, complemented by a range of domestic suppliers. Moana Technologies and other P. monodon broodstock suppliers, such as Unima, are not yet selling to the Chinese market.

In general, locally produced broodstock is expected to continue to replace imported broodstock at a significant phase. The same industry source that provides the top 30 hatchery list claims that from 2023 to 2024, broodstock imports dropped by 30-40%, and they expect broodstock imports to drop by another 50% from 2024 to 2025. If these numbers are correct, broodstock imports to China may only amount to 200,000-300,000 pieces in 2025. Future supplies to China will further face the implications of the US tariff war. Suppose the broodstock falls under the retaliatory tariffs announced by the Chinese government. In that case, supplies to China by companies such as API and Shrimp Improvement Systems, which don’t have facilities outside the US from where they could ship to China, will face headwinds, and others will fill the gap.

SyAqua

In 2022, Ocean 14 Capital acquired a controlling stake in SyAqua from the Golden Springs Group. Today, SyAqua is the world’s fastest-growing broodstock supplier. The company runs NBC and BMC in Florida and Thailand and a BMC in Indonesia. Its facility in Thailand is used to supply the domestic market and other markets in the region that have not banned imports from Thailand, such as China and some other neighboring countries. The facility in the US is used to supply the countries that do not permit import from Thailand, such as India and Indonesia. It is the only broodstock supplier offering its hatchery clients a full range of broodstock and post-larvae diets.

SyAqua has sold approximately 140,000 broodstock in 2024 and aims to sell around 200,000 in 2025. This is up from around 125,000 pieces in 2019 when I published my initial broodstock report. In recent years, SyAqua achieved remarkable growth in Thailand (from zero in 2021 to 18,000 in 2024), Indonesia (from zero in 2022 to 5,000 in 2024), and, most of all, in India (from zero in 2020 to 80,000 in 2024). The only line the company sells, its balanced line, is widely appreciated for its combination of tolerance to disease and growth. In India, the line is especially in high demand due to its perceived high tolerance to common diseases such as EHP, White Feces, and the White Spot Syndrome. The same happens in Indonesia, where farmers struggling with disease try and increasingly choose its balanced line.

In China, Syaqua's PL is primarily sold to conventional earthen ponds in the southern region with established management experience and technical expertise. Its resistance performance demonstrates superior strength, stability, and yield compared to general fast-growing strains. Additionally, Syaqua is expanding into the greenhouse farming market due to its outstanding resistance against EHP and white feces symptoms. According to the company, in China's low shrimp price market, Syaqua's commercial shrimp enables farmers to achieve higher revenues thanks to the high survival rates during live transportation.

While strategically scaling down sales in Thailand, in 2025, the company aims to grow sales in India, Indonesia, China, and Vietnam. The company claims to have one of the best genetics programs in the world and strongly believes in its methods. The company will focus on continuously improving its program and show the positive impact of its genetics on FCR, which, according to the company, is more than 20 points better than its competitors. If its plans materialize, the company will become the world’s largest third-party broodstock supplier by 2026.

Indonesia

To get a better view of the hatchery market in Indonesia, I talked to Danny Leonardo of Prima Larvae and the head of Indonesia’s hatchery association. Their perspectives are integrated into this section.

Indonesia’s hatchery association estimates that Indonesia’s production of L. vannamei PL dropped from around 32 billion in 2023 to 26 billion in 2024. Hendrix Genetics claims that in 2024, the broodstock supply dropped to 100,000 from 120,000 in 2023. According to Hendrix Genetics, it holds 70% of the market share. The rest of the market share is contributed by Shrimp Improvement Systems (10-15%), Prima Larvae (5-10%), and SyAqua (5%). Smaller suppliers in 2024 were Benchmark Shrimp Genetics, American Penaeid Inc., and Blue Genetics. Also, CP Florida has entered the Indonesian market since early 2025. The hatchery association expects that the amount of broodstock and PL sold will improve in 2025 due to improved industry conditions.

Prima Larvae Bali is the largest domestic broodstock producer, and through this supply, its hatchery operation has become self-sufficient. The company already has a breeding program and hatchery capacity to produce four billion PL. With a scheduled investment in Sulawesi and an expansion in Bali, the company's production capacity could increase to 6 billion PL over the next two years. This equals a 20-25% market share, and its breeding program significantly reduces the market for overseas broodstock suppliers.

The hatchery association argues that requirements from hatcheries and farmers are changing. The L. vannamei broodstock market is in a phase of evolution marked by supplier strategy adjustments, new production capacities, and hatchery and genetic growth protocol refinements. Also, the farming landscape is evolving with a segregation of market segments between more conventional semi-intensive farms and more innovative intensive farms. While the former requires tolerant or balanced lines, the latter often chooses fast growth lines.

Blue Genetics

In 2023, Mexico-based Blue Genetics acquired Sea Products Development in Texas. This acquisition drastically increased the company’s capacity. Today, its operations in Mexico are mainly used to develop its genetics lines (its disease-tolerant Golden Line and its new Sky Line, which has better growth rates). PPL is sent from Mexico to its BMCs in India and Thailand and to its facility in Texas. Its PPL is grown in Texas to adult broodstock and shipped to clients worldwide. In Texas, the company also maintains its fast-growing Texas line. The company now has the flexibility it needs to reach its full potential.

In 2024, Blue Genetics shipped 38,500 PPL from Mexico to its BMC in Thailand and 75,000 PPL to its BMC in India. From Texas, the company shipped XX adult broodstock. Total adult broodstock supplied to hatcheries in 2024 reached 140,000 animals.

The program in Thailand has been slowed down as Chinese customers prefer to receive animals from Texas instead of Thailand due to the poor reputation of Thai broodstock suppliers. About India, Blue Genetics struggled with the performance if its previous genetic lines. One was tolerant to disease but didnt grow fast enough, and the other grew fast but was not sufficiently tolerant to disease. In 2024, Blue Genetics shipped PPL from several lines to fine-tune the best possible genetics for the Indian market. Its new line is now being launched under the commercial name SKY LINE, and PPL and broodstock shipments are being prepared to be on time for the next crop. Blue Genetics expects this new line to regain market share in 2025 and beyond.

Blue Genetics' biggest market is in China. In 2024, the company shipped over 100,000 adult broodstock of its Golden Line of disease-tolerant animals to its customers in China, especially in the North, where farmers require broodstock that performs well amidst heavy disease pressure. In that market segment, Blue Genetics estimates it market share at around 60%. In the greenhouses in South China, farmers require fast growth lines. Blue Genetics plans to promote its Sky Line to this segment aggressively and expects to sell at least 10,000 broodstock to this market.

Blue Genetics is also selling to other markets. Last year, it entered Iran and sold thousands of broodstock from its Golden Line. In Indonesia, while numbers are still small, the company has launched its Golden and Texas lines and will launch its Sky Line later this year, enabling it to grow its sales. In Vietnam, Blue Genetics is just entering the market, focussing on its Texas line as Vietnamese farmers are focused on fast growth.

In February 2024, Groupe Grimaud, the owner of Blue Genetics, publicly announced that it wanted to sell Blue Genetics. The group's CEO is about to retire, and without a family successor lined up, he sells his shares to the other company owners. The other company owners have decided to focus the future of the group on its business for land-based animals. As a result, the group is looking to sell Blue Genetics to a strategic investor who can lead Blue Genetics to its next level of growth. Want to know more about the takeover of Blue Genetics? Contact Mr. Alex Bechu (alex.bechu@grimaud.com).

Vietnam

The total broodstock market size in Vietnam is estimated to be around 200,000 animals of which around 50,000 are produced locally and around 150,000 are imported. Rough estimates lead to the conclusion that Shrimp Improvement Systems supplies around 80,000-90,000 broodstock, Viet-Uc around 60,000-70,000 broodstock, and CP Group around 30,000-40,000 broodstock to Vietnam. The rest of the market is fragmented.

Vietnam’s broodstock market continues to be dominated by Viet-Uc, Shrimp Improvement Systems, and CP Group. Viet-Uc remains the country’s largest producer of broodstock. The company claims to have a market share of around 35% in the PL segment and is entirely self-sufficient concerning broodstock supply. It’s unclear whether the company has already started to commercialize its P. monodon breeding program or whether that is still under development. CP Group, Vietnam’s second largest PL producer, supplies P. monodon and L. vannamei broodstock from its group facilities in Thailand. The company’s hatcheries produce PL for both species. CP’s share of the total PL market is estimated to be around 15%.

Shrimp Improvement Systems is the largest supplier of L. vannamei broodstock to the hatcheries that do not have a breeding program and, as such, depend on third-party broodstock. Bill of lading data suggests that SIS holds an 85% share of imported broodstock (excluding CP Group) and 40-45% of the total broodstock market. Blue Genetics, Kona Bay, Benchmark, and API all supplied small quantities to Vietnam, but none accounted for more than 1% of total imports. Thai companies supplying to Vietnam include Top Aquaculture, SR Aquatec, and YHLF biotech, each accounting for 3-5% of total imports.

Regarding P. monodon, besides Viet Uc’s integrated breeding program and integrated supplies by CP Group, the largest supplier from overseas remains Moana Technologies from Hawaii. Moana supplies its local BMC Moana Ninh Tuan, which distributes P. monodon broodstock to local hatcheries. There are, at the moment, no other competitors, as Unima is not supplying broodstock to Vietnam yet.

API

American Penaeid Inc. has gone through rough weather in 2024. The company’s facilities in Florida were hit by two hurricanes only three weeks apart. First, Hurricane Helene, while not a direct hit, caused a remarkable amount of damage to its greenhouses, which a tornado may have hit. While picking up the pieces and repairing the facilities, three weeks later, Hurricane Mitch had a direct impact and destroyed all the greenhouse structures, essentially beyond repair. After the storm had passed, the company’s crews were immediately tasked with removing the debris from its tanks and installing individual tank covers, using the usable metal parts from the destroyed greenhouses. Because of its quick action, the company was able to winterize most of its broodstock for the upcoming broodstock season. Robin Pearl, the company’s CEO, expresses his deep appreciation for his crew, who worked tirelessly to protect the animals and ensure operational capabilities were quickly restored.

Pearl resigned shortly after this. But as quick as the CEO left, he also returned. He explains that following the impact of the last two hurricanes, the company needed emergency capital to repair the facilities. A large family shareholder group provided the capital but insisted on taking on a more active role. This quickly transformed his duties from CEO to salesman, and he resigned in November. The shareholder family could not operate the business, and very quickly, it became apparent that his role and skills were significantly more critical than they had imagined. During the nearly 2 months of his absence, they could not follow through on the many opportunities. With the loss of team, sales, and dwindling cash flow, they decided bankruptcy in January was the only way of saving the company. However, within a week from filing, the shareholders and other stakeholders demanded that Pearl return and the family step aside.

Asking Pearl what we should know about how his company will now move ahead, he acknowledges that recent years have been uniquely challenging for the company. First, Covid took the wind out of its growing international business, and then a direct hit of Hurricane Ian in late 2022 caused over $2.5M in damages. API, like most others in the industry suffered through the worst industry slump in 2023 and 2024, and then to top it all off, in late 2024, it was hit by two more hurricanes, which essentially destroyed all its greenhouses - completely writing off the $2.5 million in repairs it had just spent 2 years prior. Then, finally, internal shareholder dissent led to Robin’s resignation and eventual return. He returned because the opportunity for the business to be a major player remains as strong as ever. Pearl claims API has an excellent team, fantastic animals, and a superior location (once climate-resilient upgrades are made), and frankly, the setbacks experienced were out of its control. After some time off and a chance to disconnect and reflect, he claims to have a renewed sense of commitment and, maybe even more importantly, a renewed sense of urgency. He aims to get the company through the re-organization as quickly as possible, then refocus on reclaiming its position as leading broodstock supplier to the world and developing the US domestic shrimp supply.

Despite its challenges at the end of 2024, API shipped approximately 120,000 broodstock in 2024. About 30% to China, about 20% to SE Asia, 25% to South Asia, and 25% to Central and South America. While earlier, it was by far the largest supplier to China, today, it has lost that position. Pearl notes several causes. First, he explains that when the company shipped PPL instead of adult broodstock to China during the COVID-19 pandemic, its customers did not do the culling. Instead of using just the 10% best animals, they would use all the animals as adult broodstock. This was detrimental to the hatchery’s results, and the company’s brand took a heavy hit. Second, API was focused on the hatchery segment supplied to the conventional shrimp farms in North China, which required tolerant and robust animals due to the struggle to perform with widespread disease prevalence. However, China’s production has increasingly shifted to small indoor greenhouses, which are predominantly looking for faster growth lines, which API cannot offer. Third, Pearl reminds us of the long-term lawsuit it has engaged in with a Chinese company. As a result of the lawsuit, his counsel advised Pearl not to travel to China. Now, the ruling has been thrown out by the US Court of Appeals. In November 2024, he traveled to China for the first time in seven years. He visited customers, hatcheries, and farmers whom he had not met in person for a long time.

His recent visit and the progress API is making with the introduction of its Fire Dragon and Golden Dragon Lines make Pearl look forward to and confident about rebuilding API’s market share in China and other markets in Asia and Latin America. The Fire Dragon line includes a trait for a better absorption of astaxanthin, an antioxidant that gives the animals a red color and helps protect them from environmental challenges. The Golden Dragon line grows fast in high-density ponds, better suited for the greenhouse farms in China and more intensive farms in countries such as Vietnam and Indonesia.

Conclusion

We have seen a lot of turbulence in the broodstock supply landscape. M&A activity has led to the change in ownership of Benchmark Shrimp Genetics and Primo Broodstock. Blue Genetics and its sister company, Sea Products Development, are up for sale and will likely change ownership in 2025 or 2026. Moreover, API, still the world’s largest broodstock supplier not too long ago, has filed for bankruptcy and has to regain strength to survive.

Looking at the bigger picture, we slowly see overseas broodstock supply consolidate in a few major groups. Companies such as Hendrix Genetics, CP Group, SyAqua, and Blue Genetics are well-positioned to supply a wide range of markets with their NBCs and BMCs spread between the US and Asia. Shrimp Improvement Systems remains the largest independent broodstock supplier, and while not yet making investments in infrastructure like its competitors, it maintains its market share in most key markets.

In 2025, companies with facilities in the US may face challenges if Trump’s trade war escalates. US suppliers could face retaliatory duties. This is already the case in China, where US suppliers must pay a 15% duty. While some can shift supply to their facilities in Asia, those who don’t have this option are likely to see business with China drop. We have to wait and see how potential tariff wars may impact broodstock trade flows throughout 2025 and beyond, but some impact is expected.

The disturbance of existing trade flows may also accelerate some of the efforts in major shrimp-producing countries to reduce their dependence on overseas broodstock. This trend is most clearly visible in China, Indonesia, and Vietnam, but also in India, this trend may follow suit.